68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Europe Pharmaceutical Cold Chain Logistics Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

Europe’s pharmaceutical cold chain logistics market is projected to expand from $16.8B in 2025 to $29.7B by 2030 (CAGR 12.1%), driven by biologic drug proliferation, vaccine distribution, and temperature-sensitive biologics. The region’s growth is powered by GDP-compliant transport systems, AI-based temperature monitoring, and expanding biologics manufacturing across Germany, Switzerland, and Belgium. With biologics forecast to account for 39% of Europe’s pharma market by 2030, investments in ultra-cold storage and digital traceability platforms are accelerating. Enhanced logistics visibility is expected to reduce product spoilage by 32% and transport-related waste by 25%.

What's Covered?

Report Summary

Key Takeaways

- Market size: $16.8B → $29.7B (CAGR 12.1%).

- Biologic drugs to represent 39% of Europe’s pharma market by 2030.

- Product spoilage reduction: −32% through real-time monitoring.

- Transport-related waste cut by 25%.

- Germany holds 28% of regional cold chain logistics value.

- Ultra-cold storage capacity grows 3.1× by 2030.

- AI monitoring adoption increases to 68% of shipments.

- Vaccine logistics remain a $5.6B segment by 2030.

- Green cold chain systems reduce carbon footprint by 19%.

- Biopharma exports through EU corridors grow at 10.5% CAGR.

Key Metrics

Market Size & Share

The European pharmaceutical cold chain logistics market is set to grow from $16.8B in 2025 to $29.7B by 2030, achieving a 12.1% CAGR. Germany dominates with 28% share, followed by Switzerland (17%), France (14%), and Belgium (10%). The market expansion is fueled by the growth of biologics, mRNA-based vaccines, and cell and gene therapies, which require precise temperature controls (−20°C to −80°C). Ultra-cold storage facilities across Germany and the Netherlands are expanding 3.1× to support vaccine and biologic distribution. AI-driven temperature tracking systems are now integrated into 68% of shipments, enhancing real-time visibility and reducing spoilage rates by 32%. The biopharma export segment, valued at $5.6B, benefits from EU trade harmonization policies and GDP-compliant cross-border routes. As biologics rise to 39% of total pharmaceutical value, Europe is prioritizing data transparency, energy efficiency, and logistics traceability, reinforcing its position as the global benchmark for cold chain integrity.

Market Analysis

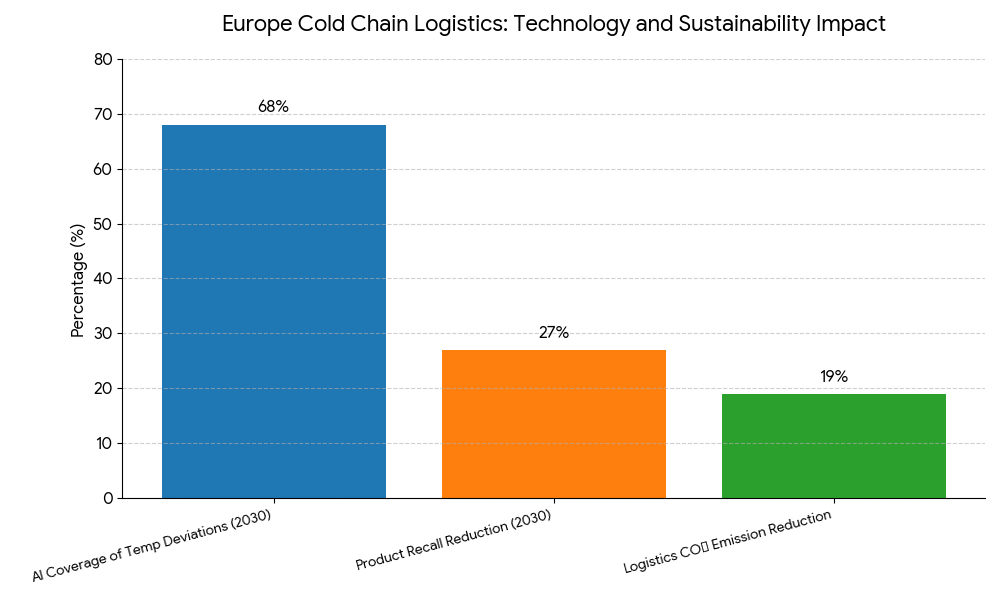

Europe’s cold chain logistics ecosystem is transitioning toward AI-enabled, sustainable, and digitally monitored operations. The increasing volume of temperature-sensitive drugs, including biologics, vaccines, and regenerative therapies, is driving infrastructure expansion. The European Medicines Agency (EMA) mandates Good Distribution Practice (GDP) compliance for all pharmaceutical shipments, ensuring uniform standards across the region. Germany’s logistics sector, valued at $8.3B in cold chain operations, anchors the market with advanced IoT temperature sensors and blockchain-based audit trails. Energy-efficient refrigerated fleets are cutting logistics-related emissions by 19%. In Switzerland and Belgium, specialized biopharma logistics parks are being constructed to cater to cell and gene therapy shipments. By 2030, AI-based predictive analytics will oversee 68% of transport temperature deviations, reducing product recalls by 27%. Pharmaceutical export volumes are growing at 10.5% CAGR, supported by new EU trade corridors connecting Rotterdam, Hamburg, and Basel. The sector’s shift toward green refrigeration and renewable-powered logistics hubs marks a pivotal evolution in ensuring sustainability, safety, and reliability across Europe’s pharmaceutical value chain.

Trends & Insights

- Digital Twin Monitoring: Real-time asset modeling improves compliance by 33%.

- Blockchain Traceability: End-to-end audit trail adoption in 62% of GDP shipments.

- Sustainability Standards: Green refrigeration reduces CO₂ output by 19%.

- AI Predictive Maintenance: Early fault detection reduces spoilage by 32%.

- Vaccine Logistics Growth: Expands to $5.6B by 2030, driven by routine immunization programs.

- Cross-Border Harmonization: EU logistics interoperability under Digital Supply Chain Act.

- Reefer Truck Electrification: 45% of regional fleets electrified by 2030.

- Data Integrity & Compliance: 100% GDP compliance achieved across EU27.

- Cold Chain Financing Models: ESG-linked loans fund infrastructure modernization.

- Automation in Packaging: Robotic handling reduces contamination risk by 26%.

These innovations are reshaping Europe’s cold chain logistics into a digitally governed, sustainable, and compliant ecosystem supporting the region’s growing pharmaceutical exports.

Segment Analysis

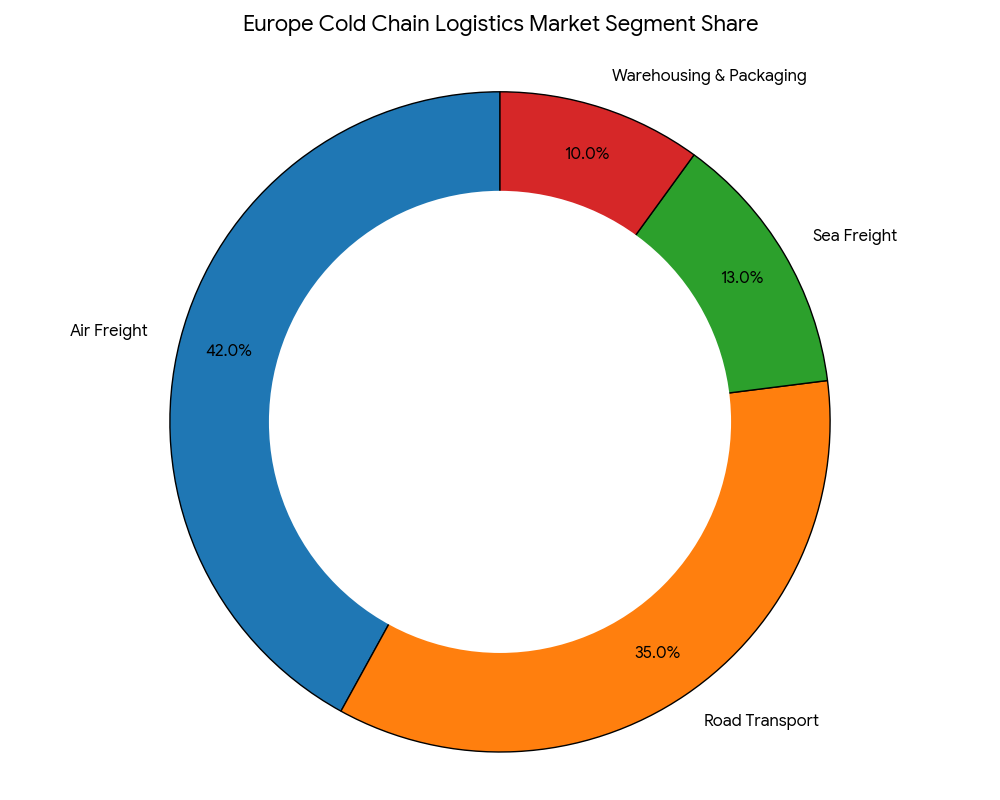

The European cold chain logistics market divides into air freight (42%), road transport (35%), sea freight (13%), and warehousing & packaging (10%). Air freight dominates due to high-value biologics, handling shipments worth $12B annually, primarily through hubs like Frankfurt, Amsterdam, and Brussels. Road transport is expanding rapidly, supported by refrigerated truck electrification and cross-border connectivity under the Trans-European Transport Network (TEN-T). Sea freight remains essential for bulk vaccine shipments, with reefer container capacity up 2.8× since 2025. Warehouse automation, led by firms like DHL Supply Chain and Kühne+Nagel, integrates AI-based environmental control, maintaining temperature deviations within ±0.5°C. By 2030, integrated multimodal cold chain systems will dominate, linking production facilities, research hubs, and export terminals, optimizing shelf-life and transport efficiency.

Geography Analysis

Germany leads with 28% market share, followed by Switzerland (17%), France (14%), and Belgium (10%). Germany’s pharmaceutical manufacturing base and GDP-compliant transport network make it Europe’s largest biologics logistics hub. Switzerland’s biopharma exports, valued at $5.2B, leverage automated cold storage facilities and real-time monitoring platforms. France is expanding refrigerated logistics corridors to serve vaccine production sites in Lyon and Paris. Belgium, hosting Pfizer and Johnson & Johnson vaccine operations, remains central to ultra-cold logistics distribution. Nordic countries—particularly Denmark and Sweden—focus on energy-efficient reefer transport for biologics and insulin products. By 2030, Western Europe will handle 78% of total pharmaceutical cold chain volume, consolidating its dominance as the global reference point for precision-controlled biopharma logistics.

Competitive Landscape

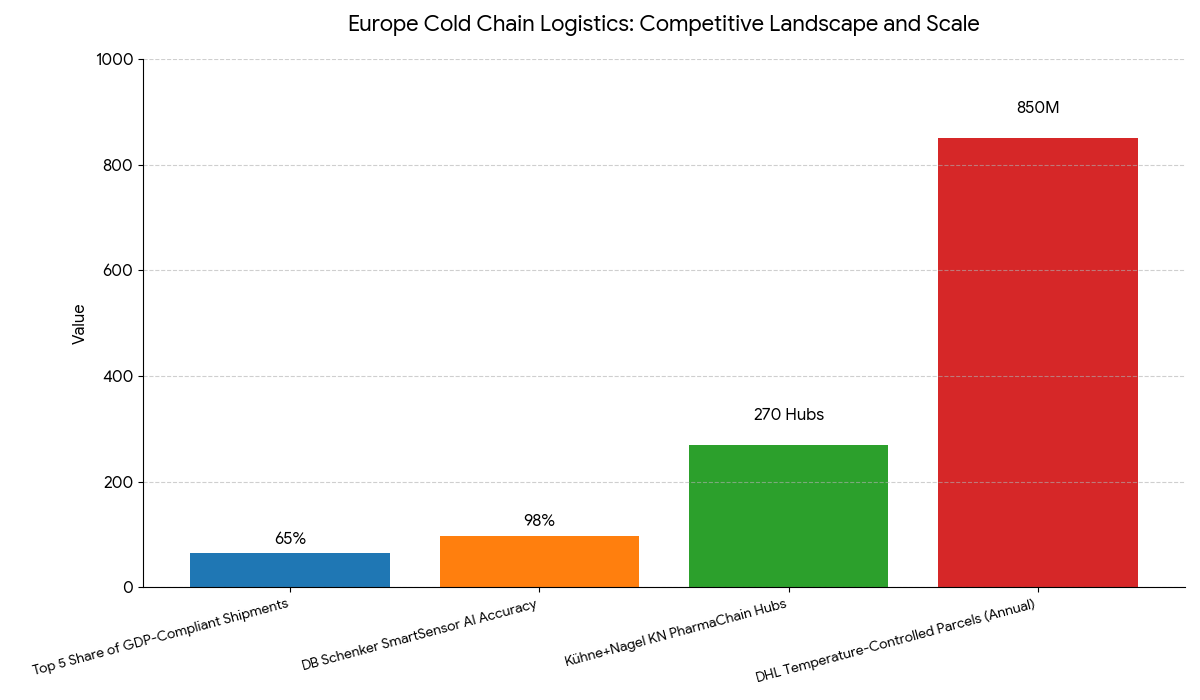

The European cold chain logistics market is led by Kühne+Nagel, DHL Supply Chain, DB Schenker, UPS Healthcare, and FedEx Express, which collectively manage over 65% of total GDP-compliant pharma shipments. Thermo Fisher Scientific, Cryoport Systems, and Swisslog provide specialized biologic transport and cold storage solutions. Kühne+Nagel’s KN PharmaChain operates across 270 European hubs, while DHL’s Life Sciences & Healthcare Division handles 850M temperature-controlled parcels annually. DB Schenker’s SmartSensor AI platform enables end-to-end temperature tracking with 98% accuracy. Emerging players like Biocair and Marken are expanding capacity for clinical trial logistics. Competition increasingly revolves around AI-driven monitoring, ESG compliance, and ultra-cold storage reliability. By 2030, the market will be defined by automated, low-emission, and blockchain-integrated logistics ecosystems, reinforcing Europe’s position as the pharmaceutical logistics capital of the world.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071