68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Energy Harvesting System, Smart Environment Application: IoT Integration & Wireless Sensor Network Optimization

Between 2025 and 2030, North American smart‑environment deployments will shift from battery‑powered endpoints to energy‑harvesting and battery‑optional nodes. The drivers are labor constraints for battery replacement, ESG goals to cut lithium waste, and the expanding feature set of ultra‑low‑power radios and sensors. In commercial buildings, campuses, healthcare, logistics, and smart cities, indoor photovoltaic (PV), thermoelectric (TEG), and vibration harvesters combined with power‑management ICs and micro‑storage (thin‑film batteries/supercapacitors) enable multi‑year maintenance‑free operation. Wireless sensor networks (WSNs) built on BLE, Zigbee/Thread, LoRaWAN, and private 5G/NB‑IoT adopt duty‑cycled and event‑driven schemes to achieve energy neutrality while maintaining data fidelity. Economically, ‘no‑truck‑roll’ operations and longer asset life transform total cost of ownership (TCO). Illustrative models show breakeven in 18–30 months for retrofits that avoid battery service, with additional savings from demand‑response, HVAC optimization, asset tracking, and safety compliance automation.

What's Covered?

Report Summary

Key Takeaways

1) Design for energy neutrality: match harvesters, storage, and duty cycles to worst‑case seasons.

2) Indoor PV + PMIC MPPT delivers the highest yield for smart‑building endpoints; TEGs excel on industrial assets.

3) Use supercapacitors for radio/inference bursts; thin‑film batteries for baseline autonomy.

4) Adopt harvesting‑aware scheduling and adaptive Tx power to maintain QoS under low‑light/ΔT dips.

5) Edge AI compresses data and lowers backhaul energy without losing detection quality.

6) Plan security from day one: secure boot, attestation, OTA, and segmented keys per device class.

7) Second‑life micro‑buffers reduce demand spikes and improve resilience during outages.

8) Procure outcomes: availability SLAs, packet delivery ratios, and energy‑budget adherence KPIs.

Key Metrics

Market Size & Share

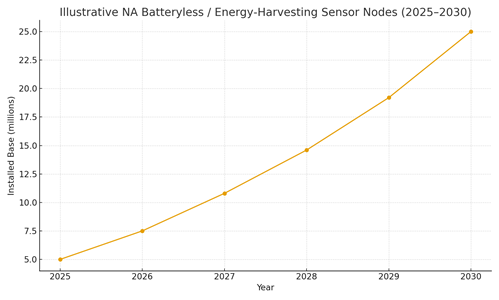

The North American market for batteryless and energy‑harvesting endpoints is expanding across smart buildings, logistics, healthcare, and smart‑city infrastructure. Our illustrative deployment curve rises from ~5 million endpoints in 2025 to ~25 million by 2030, driven by maintenance avoidance and analytics value. Smart buildings capture the largest early share thanks to predictable irradiance and occupancy‑driven use cases (HVAC optimization, IAQ, space utilization, safety). Logistics/industrial sites follow as TEG‑based and vibration harvesters mature for rotating equipment and cold‑chain assets. Municipal deployments grow with street‑level sensors and parking/lighting controls.

Share dynamics depend on (1) retrofit friction and commissioning tooling; (2) harvester yield versus ambient conditions; (3) interoperability with existing BAS/IT systems; and (4) the availability of outcome‑based service contracts that guarantee uptime and packet delivery ratios. Vendors with modular kits, validated harvester‑storage pairings, and reference firmware will capture framework agreements across multi‑site portfolios.

Market Analysis

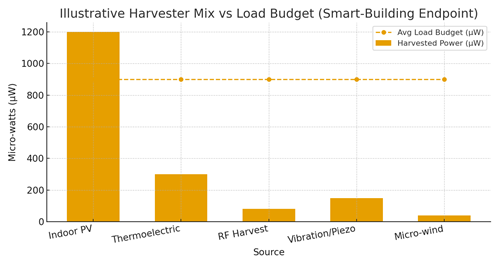

Energy neutrality is a budgeting problem: harvested power must exceed average load across seasonal minima. For smart‑building endpoints, indoor PV provides the highest average yield; TEGs excel where waste heat is available; vibration harvesters supplement low‑light zones; RF harvesting remains niche but valuable for micro‑events. Our illustrative harvester mix shows indoor PV at ~1.2 mW, comfortably above a 0.9 mW average load when coupled with adaptive duty cycling. System design should co‑optimize sensor sampling, local processing, and radio bursts, using supercapacitors for peak loads and thin‑film batteries for autonomy. Power‑management ICs with MPPT and cold‑start features are essential for reliable operation.

Economics hinge on avoided battery service, reduced downtime, and analytics‑driven savings (HVAC, lighting, asset tracking). Contracts should include energy budgets, packet‑delivery SLAs, and cybersecurity requirements. Integration with BAS/SCADA/CMMS unlocks closed‑loop control and measurable ROI.

Trends & Insights

Ultra‑low‑power MCUs and radios push sleep currents toward sub‑200 nA; AI‑enabled compression reduces transmissions while preserving detection accuracy. Standardized harvester‑storage modules simplify design‑in. Federated learning improves anomaly models without raw data export. Certification frameworks for second‑life cells support micro‑buffer warranties. Digital twins simulate energy flows per node, informing placement and firmware settings. Utility programs expand demand‑response and grid‑interactive building incentives, favoring batteryless retrofits. Security baselines (secure boot, attestation, OTA) become table stakes for enterprise adoption.

Segment Analysis

Commercial Real Estate & Campuses: focus on HVAC/IAQ, space use, and safety; prioritize BLE/Thread with indoor PV. Healthcare & Pharma: cold‑chain and compliance sensors; prefer TEG + LoRaWAN/NB‑IoT for long‑range inside campuses. Industrial & Logistics: vibration/TEG for rotating equipment and asset tracking; ruggedized enclosures and edge AI. Municipal/Smart City: street‑level sensing and lighting/parking; LoRaWAN/private 5G backbones with supercap buffers.

Geography Analysis (USA & North America)

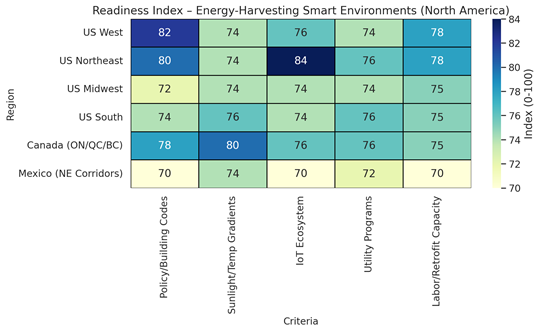

Readiness is strongest in the US West and Northeast due to policy, dense retrofit markets, and mature IoT ecosystems. The South benefits from favorable irradiance and growing utility programs; Canada’s leading provinces balance policy support with strong tech partners and address cold‑weather needs. The Midwest offers large retrofit stock but faces variable irradiance and older building stock. Mexico’s industrial corridors are emerging with strong logistics demand. Multi‑region buyers should align rollouts with building codes, utility incentives, and commissioning capacity.

Competitive Landscape

Key players span harvester OEMs (indoor PV, TEG, piezo), PMIC/storage vendors, sensor and radio module makers, WSN software platforms, system integrators, and building/industrial automation providers. Differentiation centers on validated harvester‑storage pairings, reference firmware, security posture, and integration with BAS/SCADA/CMMS. Providers offering performance‑based contracts (availability, packet‑delivery SLAs) and digital commissioning tools will gain share as portfolios scale across multi‑site enterprise deployments.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1345

$ 1432

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071