68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Digital Twin Adoption in Offshore Oil & Gas: Predictive Maintenance & Risk Mitigation Strategies

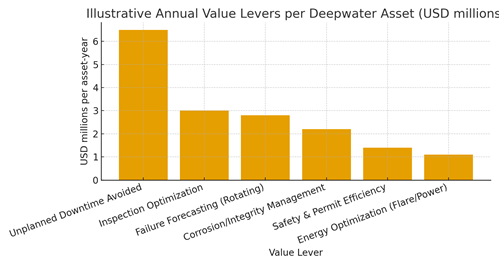

Between 2025 and 2030, offshore operators in the USA and North America will transition from pilot‑scale digital twins to platform‑level deployments focused on predictive maintenance, integrity management, and risk mitigation. A modern offshore digital twin fuses asset data (design, sensor, inspection, work orders) with physics‑based and data‑driven models to predict failure modes, optimize maintenance windows, and de‑risk safety‑critical operations. North America’s deepwater Gulf of Mexico leads adoption due to asset scale, connectivity improvements, and established integrity programs; Canada’s East Coast and Mexico’s Gulf are fast followers as data infrastructure and standards mature. The economic case centers on avoided unplanned downtime, inspection optimization, and early‑warning analytics. For a large deepwater facility, illustrative value levers point to multimillion‑dollar benefits per asset‑year: minimizing production deferment via early fault detection; risk‑based inspection that cuts rope access and subsea survey days; and corrosion/erosion models that extend run length while staying within safety margins.

What's Covered?

Report Summary

Key Takeaways

1) GoM deepwater will anchor adoption; scale and connectivity deliver outsized ROI vs. smaller shelf assets.

2) Predictive maintenance twins pay first via deferment avoidance; inspection & logistics savings follow.

3) Integrity twins (pressure systems, structures, subsea) slash risk by catching degradation earlier.

4) Standardized data models and event‑driven pipelines reduce integration time and model drift.

5) Cyber and model governance are table stakes treat twins as safety‑related software with audits.

6) Edge analytics + satellite backhaul enable near‑real‑time insights in remote fields.

7) Contract for outcomes: availability SLAs, false‑alarm limits, defect detection KPIs, and shared‑savings.

8) Scale via playbooks: start with high‑criticality equipment, then expand to fleet and multi‑asset views.

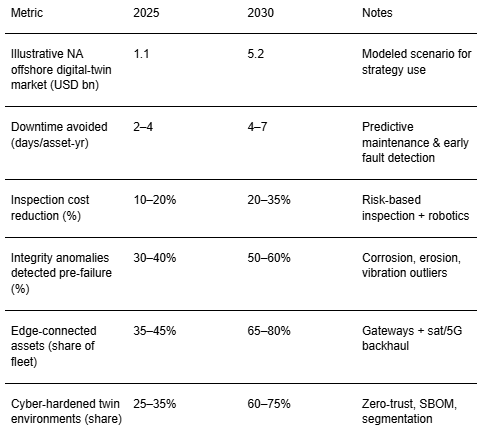

Key Metrics

Market Size & Share

North American offshore digital‑twin spend is set to grow as operators shift from pilots to multi‑asset programs. Our illustrative scenario shows a rise from about USD 1.1B in 2025 to roughly USD 5.2B by 2030. The U.S. Gulf of Mexico captures the largest share (>55% by 2030) given deepwater asset density, existing integrity frameworks, and connectivity improvements (satellite backhaul, private LTE/5G). Canada’s East Coast and Mexico’s Gulf expand next as operators consolidate data platforms and adopt standardized tags and event‑driven data pipelines. Share evolution depends on (1) production scale and criticality; (2) maturity of data and integrity programs; (3) connectivity economics; and (4) vendor ecosystems that can deliver outcome‑based SLAs.

By function, spend concentrates on predictive maintenance and integrity twins (60–65%), followed by production optimization (15–20%) and safety/risk modules (15–20%). Vendors that bundle analytics, model lifecycle management, and robotics‑enabled inspection reduce time‑to‑value and capture outsized share.

Market Analysis

The value stack for offshore twins is dominated by deferment avoidance from predictive maintenance, followed by inspection optimization and early failure forecasting for rotating equipment. Corrosion/erosion models enhance run‑length planning, while safety and permit‑to‑work efficiencies reduce exposure hours. Our illustrative value profile suggests USD 6–7M per deepwater asset‑year in avoided downtime, with an additional USD 2–3M from inspection/logistics gains. Barriers include data quality, integration costs, and cyber requirements; mitigations involve standardized tag dictionaries, historian connectors, and edge gateways that buffer and sync under intermittent links. Business‑model innovation availability SLAs, false‑alarm thresholds, and gain‑share aligns incentives and accelerates adoption.

Cost drivers: model development and calibration, data engineering, edge hardware, and robotics contracts. Over time, reusable models and shared component libraries lower unit costs, while AI‑assisted labeling and synthetic data reduce training time. The winners productize playbooks for compressor trains, subsea systems, and structural integrity, enabling repeatable outcomes across the basin.

Trends & Insights

Physics + ML hybrids dominate: simulators provide boundary‑condition realism while ML captures idiosyncratic failure signatures. Edge‑cloud symbiosis grows as gateways handle preprocessing and anomaly scoring offshore, with cloud orchestration managing models and audit logs. Robotics (ROVs, crawlers, drones) feed inspection twins, reducing exposure hours and enabling condition‑based campaigns. Model governance professionalizes with MLOps, validation against standards, and versioned SBOMs. Cybersecurity hardening (zero‑trust, micro‑segmentation) becomes mandatory, with regulator and insurer interest in auditable controls. Outcome‑based contracting spreads, with KPIs tied to deferment avoidance, inspection substitution, and safety improvements.

Segment Analysis

Majors & Supermajors: pursue fleet‑wide platforms, strict governance, and robotics integration; prioritize high‑criticality equipment first. Independents: focus on quick‑payback modules (compressors, ESPs) and managed service models to limit capex. NOCs in NA: adopt standardized playbooks and vendor bundles where deepwater assets justify scale. Service Providers/OEMs: embed twin capabilities in service contracts, offering shared‑savings and performance guarantees. Regulators/Insurers: request auditable model governance and data lineage; twin outputs begin informing risk‑based oversight.

Geography Analysis

The U.S. Gulf of Mexico leads North American adoption thanks to deepwater scale, connectivity, and mature integrity programs. Mexico’s Gulf gains momentum as data platforms consolidate and connectivity improves; Canada’s East Coast matures via standardized data and winterization‑aware models. The U.S. Atlantic has limited upstream activity; Alaska’s OCS requires specialized winterization and satellite‑first architectures. Readiness correlates with asset density, data infrastructure maturity, regulatory openness to inspection substitution, and connectivity economics.

Competitive Landscape

The ecosystem spans platform vendors, cloud providers, historian/OT data specialists, simulation houses, and robotics firms. Differentiation centers on closed‑loop integration (from anomaly to work order), physics‑ML hybrid modeling, and cyber‑assured operations. Vendors offering outcome‑based SLAs and deep domain libraries (compressors, subsea, structural) will win share. Strategic partnerships platform + robotics + inspection services accelerate time‑to‑value. As buyers scale, procurement emphasizes model governance, SBOM transparency, and portability across assets and operators.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1345

$ 1432

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071