68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Digital-Only Wealth Platforms Targeting Gen Z & Alpha: Design, Personalization, and Retention Hacks (2025–2030)

The digital-only wealth management market for Gen Z and Gen Alpha investors is projected to expand from $210B in 2025 to $470B by 2030, reflecting a CAGR of 17.5%. This growth is powered by mobile-first investing, AI-driven personalization, and gamified wealth interfaces designed for younger demographics. With 68% of Gen Z preferring digital-first advisors and trusting algorithmic recommendations over traditional advisors, platforms are leveraging behavioral finance, social investing, and micro-investment features to drive engagement. The key focus is on retention, user experience, and personalized goal tracking that align with emerging investor psychology.

What's Covered?

Report Summary

Key Takeaways

- Market size: $210B → $470B (CAGR 17.5%).

- Active digital-only users projected to reach 120M across USA & EU by 2030.

- 68% of Gen Z prefer digital-first investing channels.

- Average portfolio size to grow from $4,300 → $8,700 per user.

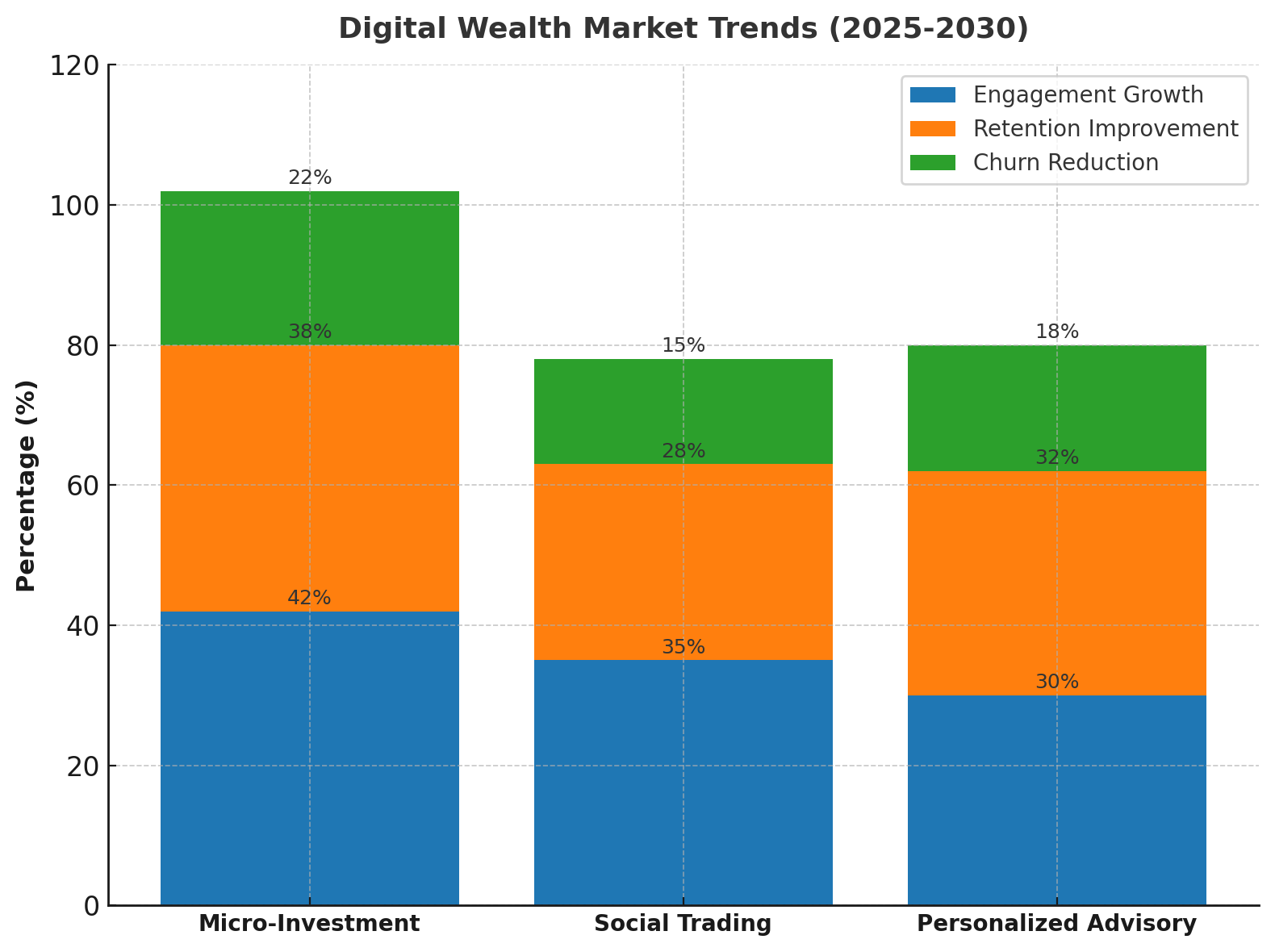

- AI personalization to lift engagement rates by 42%.

- Gamified wealth tools to improve retention by 38%.

- Robo-advisory portfolios will represent 55% of all Gen Z investments.

- Social investing features to boost referral acquisition by 33%.

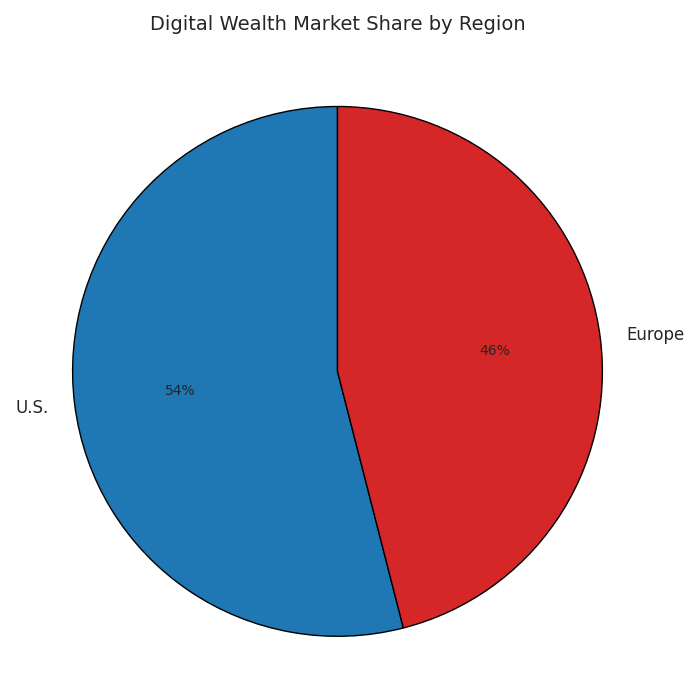

- Europe to account for 46% of global Gen Z digital investors.

- Subscription pricing models expected to cut churn by 22%.

Key Metrics

Market Size & Share

The digital-only wealth platform market in the U.S. and Europe is projected to reach $470B by 2030, up from $210B in 2025, growing at a CAGR of 17.5%. The U.S. will command 54% of market share, while Europe holds 46%, driven by increased mobile penetration, financial literacy programs, and PSD3-aligned fintech growth. The number of Gen Z and Gen Alpha investors will surpass 120 million by 2030, with an average portfolio size of $8,700, double the 2025 figure. This surge is led by the integration of AI, social investing, and micro-investment features, reducing entry barriers and enabling early wealth accumulation. Robo-advisors will dominate with a 55% market share of total managed assets in this age group.

Market Analysis

The digital wealth landscape is shifting toward user-centric personalization and data-driven engagement. Platforms are deploying AI and machine learning to tailor goal-based investment plans, resulting in 42% higher engagement and 38% improved retention. Gen Z’s expectation for instant value visualization and community-based validation has led to the rise of social trading tools, fostering peer engagement and confidence. In the U.S., platforms like Robinhood and SoFi are pioneering micro-investment gamification, while Europe’s Revolut and Trade Republic are experimenting with personalized advisory dashboards. With churn rates dropping 22% under subscription-based pricing, the focus is now on long-term portfolio growth through data transparency, regulatory alignment, and user education.

Trends & Insights

- Personalized AI Engines: Real-time investment suggestions increase engagement by 42%.

- Gamified Interfaces: Achieve 38% better retention via progress tracking and streak rewards.

- Social Investing: Peer validation boosts referral conversions by 33%.

- Financial Literacy Gamification: Raises investing frequency by 21%.

- Micro-Investment Models: Attract first-time investors under 25.

- Behavioral Nudging: Increases recurring investments by 26%.

- Sustainable Investing: ESG portfolios adopted by 64% of Gen Z users.

- Mobile-First UIs: Reduce acquisition friction by 28%.

- Voice-Enabled Interactions: 18% of users prefer AI voice recommendations.

- Creator-Led Finance Education: Platforms partnering with influencers see 30% user growth.

These trends highlight a deep cultural and technological shift from transactional investing to interactive wealth-building ecosystems.

Segment Analysis

The market divides into robo-advisory (55%), micro-investment (25%), social investing (12%), and financial literacy ecosystems (8%). Robo-advisory platforms, like Wealthfront and Nutmeg, dominate due to algorithmic precision and compliance efficiency. Micro-investment apps such as Acorns and Revolut Junior account for 25%, lowering barriers for early investors. Social investing networks, including Public.com, are capturing 12% of engagement share, emphasizing community-driven trust. Financial literacy and gamified learning tools make up 8%, serving as onboarding funnels for younger demographics. By 2030, AI and gamified wealth design will merge across all these segments, forming cohesive digital ecosystems.

Geography Analysis

The U.S. leads with 54% of the market, driven by app-based financial ecosystems and API-driven integrations. Europe, accounting for 46%, benefits from strong open banking infrastructure and youth-targeted financial reforms. The UK, Germany, and France lead adoption, while Nordic regions emphasize sustainable portfolios. European Gen Z investors show stronger preferences for subscription-based wealth models, whereas U.S. users lean toward commission-free platforms. By 2030, cross-border partnerships between U.S. and EU fintechs will drive the next phase of AI-led investment standardization, harmonizing data sharing and compliance.

Competitive Landscape

Key players include Robinhood, SoFi, Revolut, Trade Republic, Wealthfront, Betterment, and Public.com. Robinhood leads with 45% penetration among Gen Z investors, while Revolut dominates European youth adoption through multi-currency micro-investment tools. Betterment and Wealthfront specialize in goal-based AI-driven portfolios, maintaining a retention rate of 78%. Emerging competitors like Finary and Titan are developing creator-led advisory ecosystems, merging finance with entertainment. As customer acquisition costs rise, partnerships with content creators, AI chat assistants, and social finance communities will define the next growth frontier. Consolidation through acquisitions and embedded fintech integration is expected to reshape the landscape by 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071