68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Carbon Credit Pricing Strategy for Corporates: Tiered Quality Premiums & Procurement Best Practices

Corporates in the UK and Europe face a dual-market reality for carbon pricing and procurement between 2025 and 2030: compliance markets (EU ETS, UK ETS) with regulated allowance prices, caps, and free allocation reforms; and the voluntary carbon market (VCM), where quality differentiation and claims integrity determine viable price premiums. A resilient corporate pricing strategy blends both hedging compliance exposure while building a portfolio of high‑integrity voluntary credits that aligns with credible claims frameworks and science‑based targets. On the compliance side, reforms and tightening caps in the EU ETS and UK ETS underpin structurally firmer prices. Price convergence could accelerate if linkage proceeds, while EU free allocation phase‑downs and UK scope expansions alter exposure for industrials and aviation. Forward curves and internal shadow‑pricing should incorporate allowance cost trajectories, sector benchmarks, and carbon leakage safeguards. For aviation, CORSIA obligations add another layer for international routes.

What's Covered?

Report Summary

Key Takeaways

1) Treat EU ETS/UK ETS as the baseline carbon cost; use shadow prices for investment screening and hedging.

2) Adopt tiered VCM quality bands: engineered removals > high‑integrity nature‑based > other reductions with robust MRV.

3) Use ICVCM CCPs and VCMI Claims to anchor integrity and corporate claims governance.

4) Structure long‑term offtake for removals with price collars and quality ratchets to manage delivery and integrity risk.

5) Develop Article 6–compatible procurement options to future‑proof cross‑border claims where feasible.

6) Map sector exposure (aviation, power, materials, FMCG) and align procurement cadence to compliance cycles.

7) Integrate SBTi BVCM guidance to separate emissions reductions vs. beyond‑value‑chain contributions.

8) Institutionalize reputational risk controls (avoid double counting, credible MRV, registry checks, litigation‑ready records).

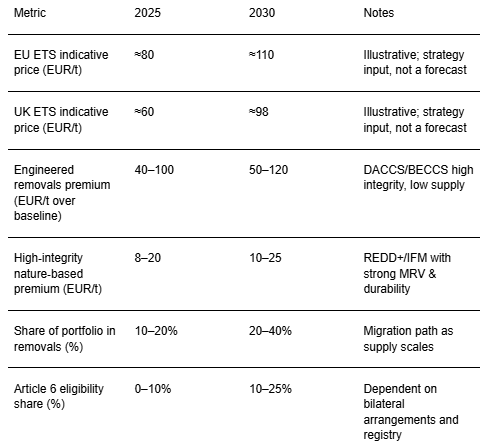

Key Metrics

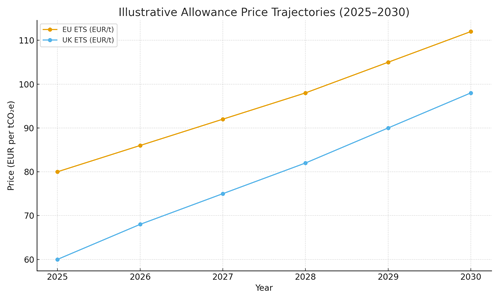

Market Size & Price Outlook (Compliance & Voluntary)

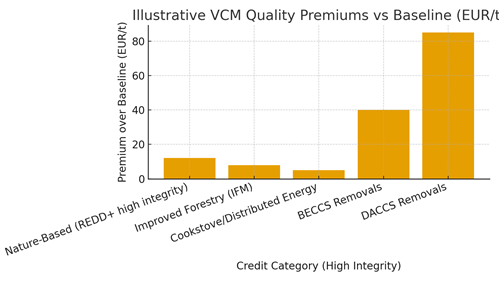

Compliance price signals in the EU ETS and UK ETS underpin the baseline cost of carbon for corporates operating in Europe and the UK. Illustrative trajectories through 2030 reflect tighter caps, reforms to free allocation, and policy discussions on potential UK–EU linkage. In parallel, the voluntary carbon market exhibits a widening quality‑based price dispersion: high‑integrity engineered removals command sizeable premiums relative to a mid‑grade baseline; high‑integrity nature‑based credits price in the mid‑tier, with spread driven by additionality, permanence, and MRV strength. Corporate strategies therefore model both regulated allowance exposures and VCM quality tiers to budget carbon costs and shape claim‑ready portfolios. A diversified approach hedging ETS obligations while gradually increasing removals exposure balances cost optimization with reputational durability.

Market Analysis (Tiered Quality Premiums)

Quality tiering in the VCM is consolidating around integrity benchmarks. Credits that meet Core Carbon Principles and support VCMI‑credible claims fetch higher prices, with engineered removals (DACCS, BECCS) at the top due to verifiable additionality and permanence but constrained supply. Nature‑based credits with high‑quality baselines (e.g., REDD+ with conservative baselines and long‑term monitoring, improved forest management) price in the mid‑tier, while household energy and distributed solutions provide cost‑effective reductions where MRV is strong. For procurement, corporates can set banded willingness‑to‑pay thresholds per tier and use contract features such as replacement rights, integrity ratchets, and buffers to manage quality drift. Over 2025–2030, we expect premium differentials to persist as integrity infrastructure scales, methodologies are reassessed, and Article 6 alignment improves the claims landscape.

Trends & Insights (2025–2030)

Policy tightening in the EU ETS and UK ETS maintains structurally firm allowance prices; potential linkage could narrow spreads and simplify compliance. Integrity frameworks (ICVCM CCPs, VCMI Claims) become the default screen for corporate buyers; registries and methodologies undergo deeper scrutiny. Article 6 authorization and corresponding adjustments gain traction for select bilateral flows, enabling more robust cross‑border claims. Buyers increasingly separate decarbonization (internal and value‑chain reductions) from beyond‑value‑chain contributions per SBTi’s BVCM guidance, while aviation CORSIA creates a distinct, standardized demand channel. Data infrastructure improves (ratings, meta‑registries), facilitating portfolio analytics, forward procurement, and risk‑based pricing. Expect continued litigation and media scrutiny, elevating the importance of transparent claims governance.

Segment Analysis (Corporate Profiles)

Aviation: Dual exposure to EU ETS/UK ETS (intra‑EU/UK) and CORSIA (international); structured hedging and standardized eligible credit pools are pivotal. Power & Heavy Industry: High allowance exposure under EU ETS; procurement focuses on hedging strategies, leakage safeguards, and potential CBAM interfaces. FMCG/Retail: Lower direct ETS exposure but significant reputational and supply‑chain pressure; favor diversified VCM portfolios with credible claims paths. Financial Services: Portfolio‑level financed‑emissions targets drive demand for credible contributions and removals offtake; require strong assurance trails. Transport & Logistics: Mixed exposure; CI‑reduction claims and SAF credit strategies may link to voluntary claims and sector programs.

Geography Analysis (UK & Europe Readiness)

Readiness for high‑integrity procurement varies across the UK and European subregions. The UK and Germany score highly on disclosure norms, market access, and policy alignment, with growing integrity infrastructure (ratings, due diligence, assurance). Nordics and Benelux show strong governance and buyer sophistication; France maintains robust policy alignment but has heterogeneous market access by sector. Southern Europe and CEE are improving but still trail on integrity infrastructure and market depth. Buyers with multi‑region footprints should calibrate procurement cadence and claims governance to local stakeholder expectations and reporting regimes.

.png)

Competitive Landscape (Ecosystem & Intermediaries)

Ecosystem participants include: (1) standards and governance bodies (ICVCM, VCMI, UNFCCC Article 6 frameworks); (2) registries and methodologies (e.g., Verra, Gold Standard, ART) undergoing integrity upgrades; (3) exchanges, brokers, and rating agencies providing liquidity and transparency; (4) developers across nature‑based, energy, and engineered removals; and (5) auditors/assurance providers. Competitive differentiation centers on integrity alignment, delivery track record, and data transparency. Corporate buyers increasingly prefer structured offtake with price collars, step‑up quality clauses, and replacement rights to manage delivery risk. As linkage discussions evolve (e.g., UK–EU ETS), compliance price signals may partially converge; meanwhile, VCM price dispersion persists due to quality stratification.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1345

$ 1432

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071