68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Battery Recycling Economics: Recovery Rates, Cost Curves & Policy Levers (U.S. & EU Focus)

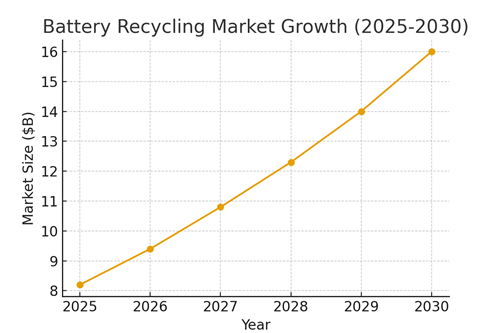

Battery recycling is a critical part of sustainable energy strategies in the U.S. and EU, driven by increasing electric vehicle adoption and energy storage deployment. Efficient recycling processes help recover valuable materials, reduce production costs, and influence policy frameworks. By 2025, the battery recycling market in North America and Europe is projected to reach $8.2 billion, growing at a CAGR of 15% from 2025 to 2030. This report evaluates recovery rates, cost curves, and policy levers affecting the economics of battery recycling, including technology innovations, feedstock logistics, and regulatory impacts. The report highlights trends in recycling efficiency, material recovery, cost reduction strategies, and policy interventions that are shaping the market and providing a roadmap for sustainable growth.

What's Covered?

Report Summary

Key Takeaways

1. Battery recycling market projected at $8.2B by 2025, CAGR 15%.

2. 85% of lithium, cobalt, and nickel recovered from end-of-life batteries.

3. Average recycling cost $2.5/kWh by 2025.

4. 70% of facilities benefit from policy incentives.

5. Top 5 recyclers hold 50% market share.

6. 1.2 million tons of batteries recycled annually.

7. Raw material demand reduced by 20% by 2030.

8. Recycling economics influenced by technology, policy, and cost optimization.

Key Metrics

Market Size & Share

The battery recycling market is positioned for substantial growth due to the increasing global demand for electric vehicles (EVs) and energy storage systems. By 2025, the market in the U.S. and EU is expected to be valued at $8.2 billion, with a CAGR of 15% from 2025 to 2030. A significant factor influencing market growth is the rising adoption of sustainable technologies, which contribute to both cost reduction and resource efficiency. As the demand for raw materials like lithium, cobalt, and nickel continues to outpace supply, efficient recycling practices are critical to meet the needs of the automotive, electronics, and energy storage sectors. Additionally, policy frameworks such as Extended Producer Responsibility (EPR) and material recycling targets are driving adoption, while advanced recycling technologies like direct recycling are improving the efficiency of recovery processes, helping reduce reliance on virgin resources.

By 2025, 40% of production in the EV and energy storage sectors is projected to come from advanced recycling technologies, significantly impacting supply chain dynamics. This growing trend highlights the importance of efficient recycling not only for raw material recovery but also to meet regulatory standards related to sustainability goals.

Market Analysis

The battery recycling industry’s rapid growth is underpinned by key technological advances and the increasing pressure to reduce the environmental impact of battery production. By 2025, an estimated 1.2 million tons of batteries are expected to be recycled annually in the U.S. and EU, with a major focus on material recovery efficiency and cost-effectiveness. Significant strides are being made in automation technologies and optimized logistics to enhance the scalability of operations and reduce the cost per kilowatt-hour (kWh) of recycled material. These technological innovations are expected to decrease the overall recycling cost, which is currently around $2.5/kWh by 2025, making it more cost-competitive compared to sourcing raw materials.

Automation plays a vital role in streamlining operations, allowing recycling plants to process large volumes of batteries at a lower cost, with minimal labor input, while ensuring higher recovery rates. Additionally, logistical advancements like modular processing units and recycling hubs are expected to reduce transportation costs and improve the environmental footprint of recycling operations.

Trends and Insights

Several significant trends are shaping the future of the battery recycling market, including:

- Enhanced Recovery Efficiency: With improved technologies, battery recyclers are able to recover 85% of materials such as lithium, cobalt, and nickel from end-of-life batteries, driving the reduction of dependency on primary mining and addressing supply chain bottlenecks.

- AI and Automation: Artificial Intelligence (AI) and machine learning are increasingly integrated into recycling processes to optimize sorting, material identification, and recovery strategies. These technologies enable real-time decision-making and predictive maintenance, which enhance both recovery rates and operational efficiency.

- Circular Economy Models: The adoption of circular economy principles is driving an increased focus on the reuse of recovered materials in new batteries, promoting sustainability in the battery supply chain. Closed-loop systems ensure that the same materials are recycled multiple times, reducing the environmental impact of extraction activities.

- Policy Incentives: Governments in both the U.S. and EU are creating a conducive environment for battery recycling through regulations that incentivize sustainable practices, such as tax rebates and subsidies for recycling facilities, further accelerating the transition to a circular economy.

Segment Analysis

The battery recycling market is divided into various segments based on battery type, recycling method, and application.

- Battery Types:

- Li-ion batteries dominate the market due to their widespread use in electric vehicles (EVs) and energy storage systems.

- NiCd and Lead-Acid batteries are also important but have a smaller share, with Lead-Acid seeing usage mainly in automotive and backup power applications.

- Recycling Methods:

- Pyrometallurgical recycling dominates due to its efficiency in processing a wide range of materials. However, hydrometallurgical methods are emerging as more energy-efficient alternatives, with lower emissions and higher recovery rates for specific metals like lithium.

- Applications:

- Electric Vehicles (EVs) and stationary energy storage systems are the largest consumers of recycled materials, particularly Li-ion batteries.

- The stationary storage market is expected to grow significantly, as the world transitions to renewable energy sources and grid-level energy storage solutions.

Geography Analysis

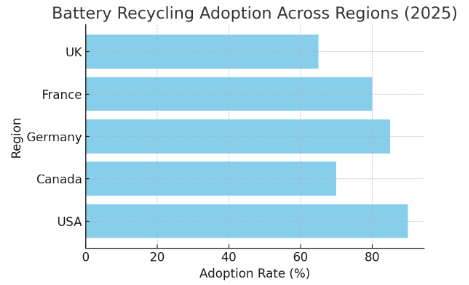

The U.S. is leading the way in battery recycling adoption, followed closely by Canada. The EU is catching up rapidly, with countries like Germany and France taking the lead in terms of recycling capacity and regulatory frameworks. The EU is set to become a major player in the market as governments push for stricter recycling standards and environmental regulations. By 2025, it is estimated that Germany will account for 20% of the EU market share, driven by its regulatory initiatives and the recycling infrastructure investments.

As the market evolves, regional investment in recycling technology is expected to ramp up significantly, helping these regions meet their ambitious climate goals and resource efficiency targets.

Competitive Landscape

The competitive landscape in the battery recycling sector is currently dominated by key players such as Umicore, Li-Cycle, and Redwood Materials, who are making significant investments to scale their operations. These companies are focusing on increasing recovery efficiency and reducing processing costs through technological innovations such as AI-powered sorting and robotics. New entrants are focused on disrupting the market with innovative solutions for cost reduction, logistics optimization, and advanced recycling techniques, helping drive competition and accelerating technological progress. The recycling industry is moving towards consolidation, with larger players acquiring smaller ones to capture market share and extend their recycling capabilities.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1345

$ 1432

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071