68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Banking as a Service (BaaS) Platform Security: Third-Party Risk Management & Compliance Automation - Risk Assessment

The Banking-as-a-Service (BaaS) sector in North America is expanding rapidly, with banks increasingly offering services to third-party companies through open APIs. By 2025, the market is projected to reach $11.5 billion, growing at 15% annually through 2030. This surge is driving demand for advanced security and compliance automation to manage third-party risks and regulatory obligations. The report highlights the importance of robust risk management frameworks and compliance technologies in shaping the future of BaaS in North America.

What's Covered?

Report Summary

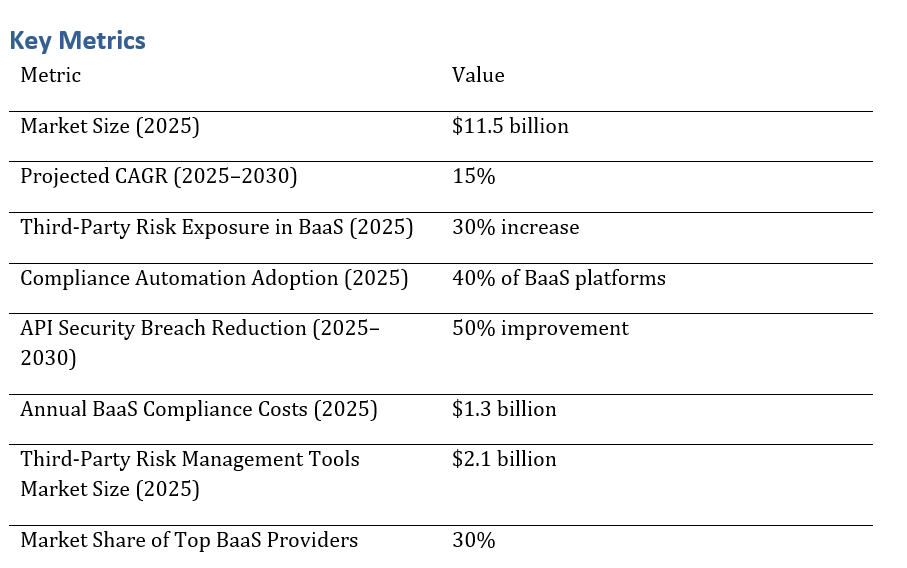

Key Takeaways

- BaaS platforms in North America are projected to reach $11.5 billion by 2025, with a growing emphasis on third-party risk management and compliance automation.

- The adoption of API security measures and compliance automation in BaaS platforms will increase significantly, with 40% of platforms expected to adopt these solutions by 2025.

- Third-party risk exposure for BaaS platforms is expected to increase by 30% by 2025, making robust security and compliance tools essential.

- By 2030, BaaS platforms will see a 50% reduction in API security breaches as security technologies improve.

- The market for third-party risk management tools is expected to grow to $2.1 billion by 2025, reflecting the increasing need for better oversight in BaaS ecosystems.

- Compliance automation will help reduce annual compliance costs by over $500 million for BaaS platforms, helping institutions save on manual compliance tasks.

- By 2030, 30% of the North American BaaS market will be controlled by the top BaaS providers, as they adopt industry-leading security measures.

- The regulatory landscape will continue to evolve, pushing BaaS platforms to integrate more robust compliance and security solutions to meet the new requirements.

a. Market Size & Share

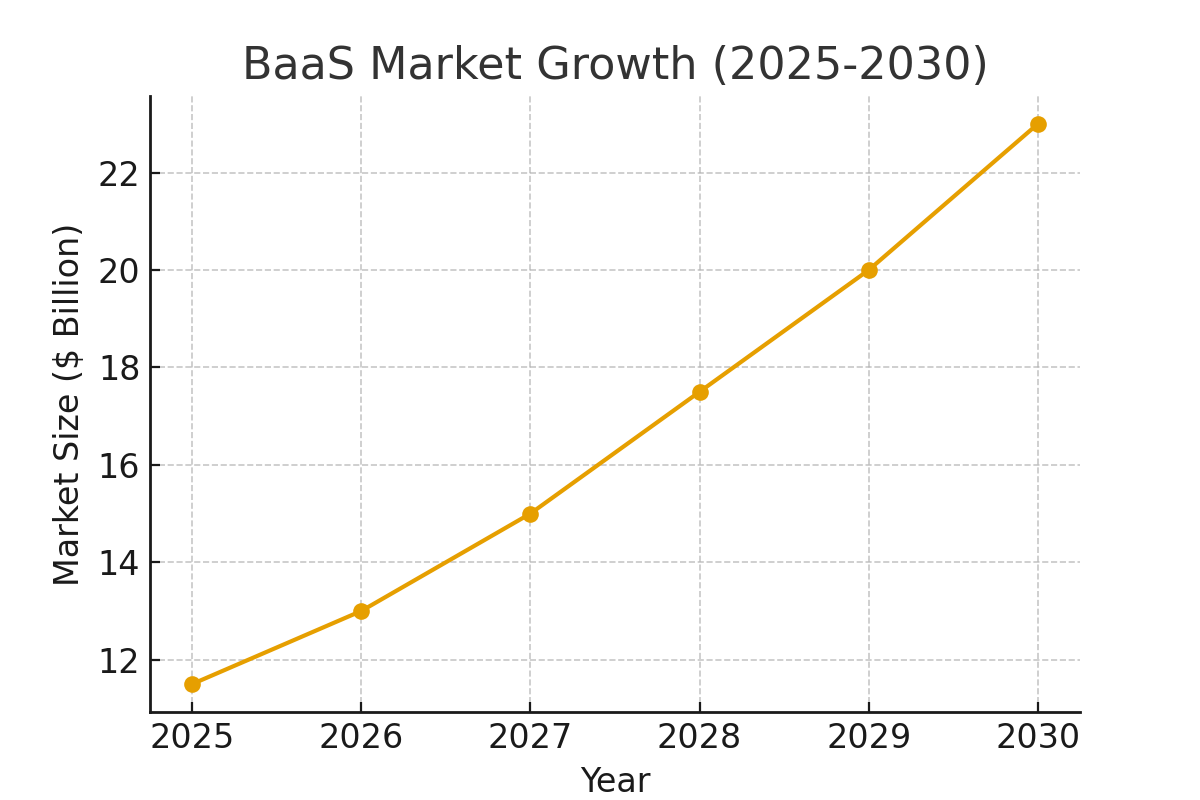

The market for BaaS platforms in North America is expected to grow rapidly, reaching $11.5 billion by 2025, with a CAGR of 15% from 2025 to 2030. This growth is driven by the increasing demand for digital banking services, the rise of open banking, and the growing adoption of API-driven platforms.

The need for enhanced security and compliance measures is critical to the growth of BaaS platforms, as institutions must mitigate third-party risks and comply with increasingly stringent regulations. By 2030, it is expected that 40% of BaaS platforms will have implemented automated compliance solutions.

BaaS Market Growth Projection (2025-2030):

b. Market Analysis

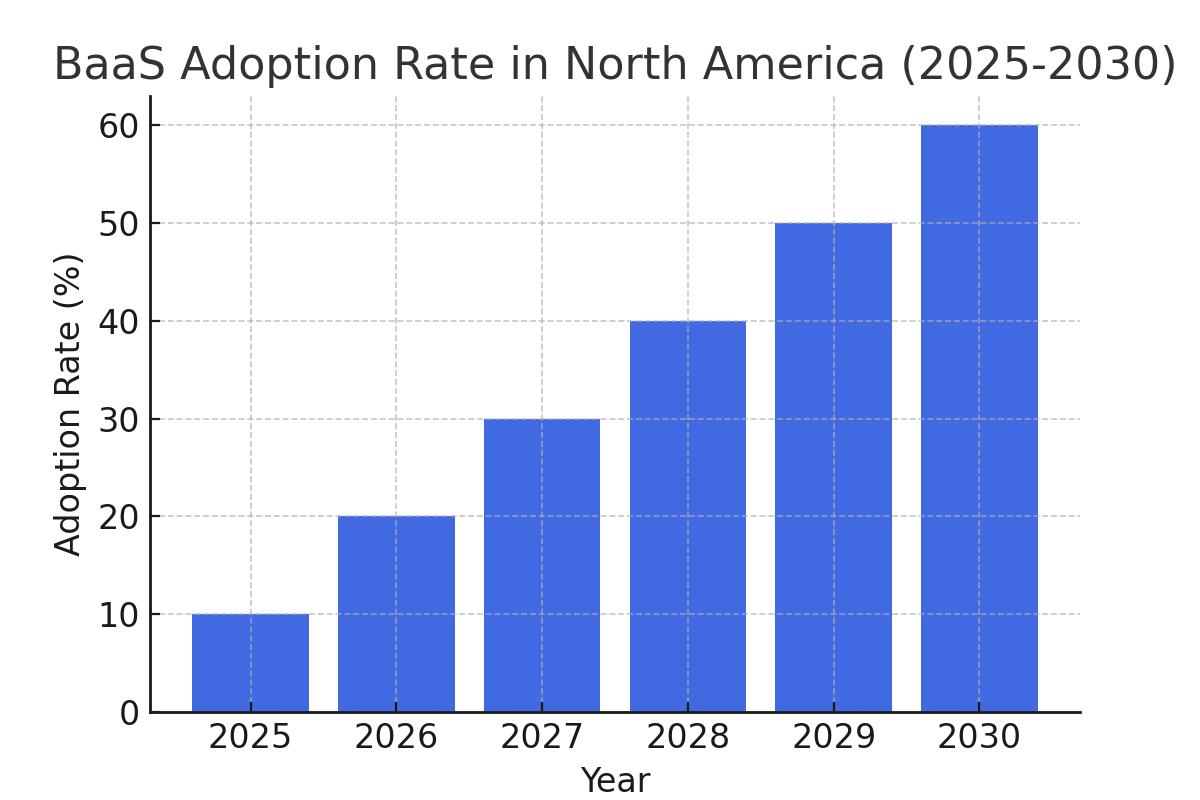

The adoption of BaaS platforms is growing rapidly in North America, driven by the demand for more flexible banking services and enhanced customer experiences. The integration of third-party APIs and open banking protocols is fueling the growth of BaaS ecosystems, with more financial institutions partnering with fintechs to create innovative services.

Compliance automation is a key component of the BaaS platform adoption cycle, helping institutions to reduce operational costs and maintain regulatory compliance with evolving standards such as PSD2, GDPR, and AML regulations.

BaaS Adoption Rate in North America (2025-2030):

c. Trends and Insights

Key trends driving BaaS adoption in North America include the increasing reliance on open APIs to expand banking services, as well as the growing focus on reducing third-party risk and ensuring compliance with regulations. Financial institutions are leveraging BaaS platforms to rapidly roll out new products and services, and to provide enhanced user experiences through collaboration with fintechs and third-party developers.

Increased investment in regulatory compliance tools and automation is expected to result in 50% fewer API security breaches over the next five years, as these platforms become more secure and compliant.

d. Segment Analysis

The largest adopters of BaaS in North America are banks, credit unions, and fintech firms. These institutions are driving the demand for flexible and scalable banking solutions through API-driven platforms. However, adoption rates vary across sectors, with fintech firms being the most agile in adopting BaaS solutions.

Smaller financial institutions are also adopting BaaS platforms at a slower pace, but are increasingly exploring these models to keep up with digital transformation trends and reduce costs associated with traditional banking systems.

e. Geography Analysis

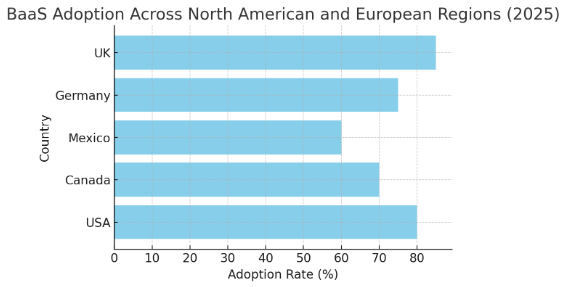

In the USA, BaaS adoption is concentrated in financial hubs such as New York, California, and Texas, where fintech and banking innovation is thriving. Europe is also experiencing rapid adoption, particularly in the UK and Germany, which have strong regulatory frameworks supporting open banking and API-driven models.

Regions in North America with high-tech penetration, like Silicon Valley, are expected to lead the charge in BaaS adoption, with increased market penetration in southern and midwestern states as awareness of BaaS benefits grows.

BaaS Adoption Across Regions (2025):

f. Competitive Landscape

The competitive landscape for BaaS in North America is dominated by large financial institutions like JPMorgan Chase, Goldman Sachs, and Citigroup, who are leveraging BaaS platforms to create new revenue streams and expand their product offerings. Additionally, fintech giants like Stripe, Square, and Plaid are making significant strides in offering BaaS services, positioning themselves as competitors to traditional banks.

Startups in the BaaS space, such as Synapse and Railsbank, are disrupting traditional banking models with more agile, scalable, and cost-effective solutions that are appealing to smaller financial institutions and fintech companies.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071