68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Phygital Retail Integration: AR Mirror Implementation & Customer Journey Mapping in Luxury Boutiques

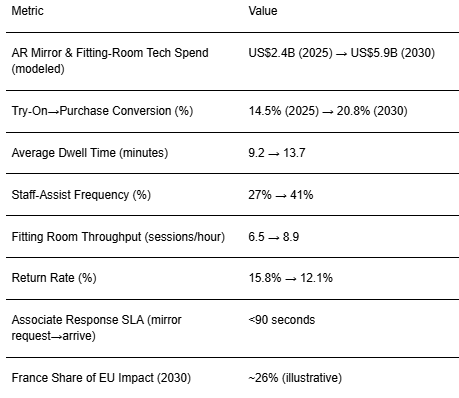

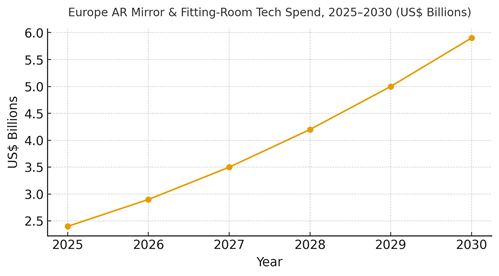

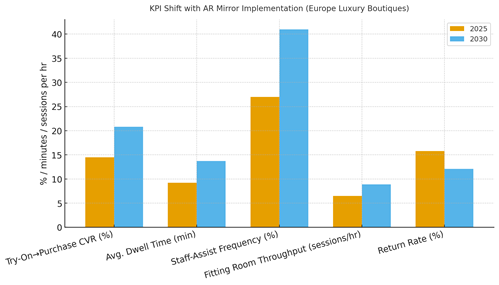

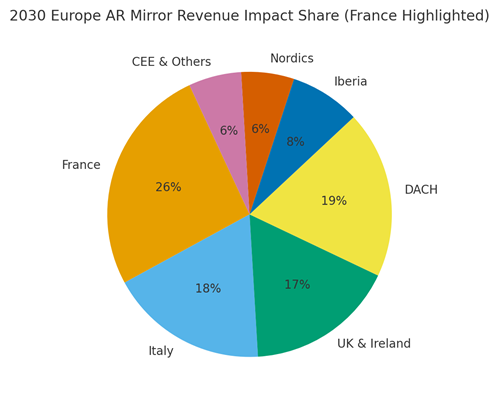

Luxury boutiques are turning fitting rooms into data-rich showrooms. From 2025 to 2030, Europe’s leaders deploy augmented‑reality (AR) mirrors and journey mapping to connect discovery, try‑on, checkout, and post‑purchase service. We model EU spending on AR mirrors and fitting‑room tech growing from ~US$2.4B in 2025 to ~US$5.9B by 2030. France leads on experiential design and boutique density, linking store theatrics with measurable outcomes. AR mirrors now function as clienteling consoles: body‑aware overlays, curated looks, and one‑tap size/color requests. Journey mapping stitches signals across POS, appointment apps, CRM, and clienteling. The result is higher try‑on→purchase conversion, longer dwell, greater staff‑assist frequency, faster throughput, and lower returns via better fit/expectations. But value arrives only with disciplined ops: calibrated lighting/cameras, privacy‑by‑design, reliable sizing recommendations, and fast associate response. KPI guardrails matter. Median programs can plausibly lift try‑on→purchase CVR from ~14.5% to ~20.8%, dwell from ~9.2 to ~13.7 minutes, staff‑assist frequency from ~27% to ~41%, and throughput from ~6.5 to ~8.9 sessions/hour while reducing return rates from ~15.8% to ~12.1% by 2030.

What's Covered?

Report Summary

Key Takeaways

1. Design mirrors as clienteling consoles, not gadgets staff workflows drive ROI.

2. Map journeys end‑to‑end; measure conversion and returns by step, not channel.

3. Fit intelligence and alterations reduce returns and increase confidence.

4. Accessibility & privacy by design: comfort modes, consent, and clear retention limits.

5. Associate response SLAs (<90s) sustain momentum and satisfaction.

6. Visual merchandising + AR scenes increase dwell and attachment sales.

7. France advantage: atelier services and cultural partnerships elevate experience.

8. CFO dashboard: try‑on→purchase CVR, dwell, staff‑assist %, throughput, return %.

Key Metrics

Market Size & Share

EU AR mirror and fitting‑room tech spend is modeled to expand from ~US$2.4B in 2025 to ~US$5.9B by 2030 as boutiques prioritize measurable experience over generic digitalization. France leads with ~26% impact share by 2030, driven by maison density and service ladders (personalization, repair, appointments). The line figure shows the compounded trajectory. Categories with high try‑on dependence RTW, footwear, leather goods capture the earliest gains; beauty benefits through regimen guidance and sampling prompts.

Share dynamics: brands with integrated inventory and clienteling gain the most, since AR prompts convert only when fulfillment is fast and accurate. Execution risks include camera sensitivity and fit bias. Mitigations: diverse training data, lighting calibration, and human‑in‑the‑loop fitting advice. Measurement must cover try‑on→purchase CVR, dwell, staff‑assist %, throughput, and return % by boutique to validate ROI alongside brand equity.

Market Analysis

AR mirrors shift store performance when tied to staff workflows and inventory. We model try‑on→purchase CVR improving from ~14.5% to ~20.8%; dwell time from ~9.2 to ~13.7 minutes; staff‑assist frequency from ~27% to ~41%; throughput from ~6.5 to ~8.9 sessions/hour; and return rate falling from ~15.8% to ~12.1% by 2030. Enablers: accurate body/fit guidance, quick size/color retrieval, appointment integration, and frictionless checkout. Barriers: hardware uptime, privacy concerns, and inconsistent lighting.

Financial lens: attribute to incremental margin after returns and staffing; model capex/opex amortization; and quantify exchange vs refund outcomes. The bar chart summarizes directional shifts when AR mirrors operate within a disciplined phygital journey.

Trends & Insights

1) AR as clienteling: mirrors surface curated looks and service options; staff convert. 2) Privacy by default: opt‑in capture, session‑local processing, and short retention. 3) Fit intelligence: body‑aware sizing and alteration prompts reduce returns. 4) Appointment‑led flows: scenes and stock pre‑staged for clients. 5) Edge compute + remote diagnostics: uptime and latency resilience. 6) Accessibility: comfort modes, captions, and alternative flows. 7) Scene experimentation: weekly tests for prompts, layouts, and lighting. 8) Omnichannel links: wishlists, one‑tap orders, and home delivery. 9) Sustainable ops: fewer unnecessary try‑ons and smarter returns. 10) Measurement discipline: CVR, dwell, staff‑assist %, throughput, return %.

Segment Analysis

RTW & Couture: Scenes for silhouettes and personalization; alteration guidance. Leather Goods: Pairing suggestions and personalization credits. Footwear: fit and gait cues; size exchanges. Beauty: shade match and regimen guidance with sampling. Jewelry & Watches: AR scale previews; appointment hand‑offs. Across segments, define prompts, consent defaults, and staff SLAs; track segment‑level CVR, dwell, throughput, and return % to guide investment.

Geography Analysis

France is projected to capture ~26% of Europe’s AR mirror revenue impact by 2030, followed by DACH (~19%), Italy (~18%), UK & Ireland (~17%), Iberia (~8%), Nordics (~6%), and CEE & Others (~6%). Paris anchors flagship rollouts; regional boutiques translate AR into service and alterations. Localization: French language assets, cultural styling, consent signage, and accessibility norms. The pie figure reflects the regional mix.

Execution: centralize analytics and content templates; let boutiques adapt scenes and staffing. Measure geography‑specific CVR, dwell, staff‑assist %, throughput, and return %; tune SLAs to store density and traffic patterns.

Competitive Landscape

Incumbents pair boutique networks and clienteling depth with premium hardware; challengers compete on computer vision, edge compute, and analytics UX. Differentiation vectors: (1) fit accuracy and lighting resilience, (2) associate workflow integration, (3) privacy/accessibility compliance, (4) inventory and alterations integration, and (5) remote monitoring uptime. Procurement guidance: demand open APIs, privacy‑by‑design certifications, hardware SLAs, and proof of incremental margin after returns. Competitive KPIs: try‑on→purchase CVR, dwell, staff‑assist %, throughput, return %, and NPS.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071