68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Hyperloop Feasibility Study: Regional Analysis of India's High-Speed Cargo Networks

India’s Hyperloop cargo transport market feasibility is gaining momentum as policymakers explore high-speed, zero-emission logistics networks capable of reshaping interstate cargo flows. The sector’s projected investment potential stands at $12.4B by 2030, with expected cargo transit speeds of 900–1,000 km/h. Pilot projects between Mumbai–Pune and Delhi–Jaipur could reduce transit times by 85% and logistics costs by 38%. By 2030, the integration of AI-driven routing, magnetic levitation, and renewable power systems could cut CO₂ emissions by 60% compared to conventional trucking.

What's Covered?

Report Summary

Key Takeaways

- $12.4B investment potential in India’s Hyperloop cargo feasibility projects.

- Transit speed: 900–1,000 km/h; travel time reduced by 85%.

- CO₂ emissions cut by 60% vs. road freight.

- Logistics costs decline by 38% with Hyperloop adoption.

- Freight volume projected at 12.5M tons annually by 2030.

- Pilot routes: Mumbai–Pune (150 km) and Delhi–Jaipur (270 km).

- Energy source: 100% renewable grid integration in feasibility design.

- Infrastructure cost: $45–$55M per km (pilot corridor estimate).

- Private–public funding ratio: 60:40 across Hyperloop initiatives.

- Asia-Pacific market share: India to represent 47% of regional Hyperloop R&D by 2030.

Key Metrics

Market Size & Share

India’s Hyperloop cargo feasibility initiatives are estimated to mobilize $12.4B in investment by 2030, capturing 47% of the Asia-Pacific R&D market. Pilot routes—including Mumbai–Pune (150 km) and Delhi–Jaipur (270 km)—are under active study by Virgin Hyperloop, Tata Projects, and DP World. Freight throughput is projected to reach 12.5 million tons annually, reducing cargo transit times by 85% compared to road haulage. The total logistics cost reduction could reach 38%, with a projected CAGR of 24.8% in Hyperloop feasibility investments. India’s manufacturing and e-commerce clusters—Pune, NCR, Ahmedabad, and Bengaluru—are being evaluated for terminal integration. The infrastructure cost per kilometer, currently estimated at $45–$55M, includes tube construction, propulsion, and vacuum management systems. The government’s National Logistics Policy (NLP) and PM Gati Shakti initiative are aligning with Hyperloop’s long-term role in decarbonizing transport corridors while advancing ESG-aligned logistics modernization across South Asia.

Market Analysis

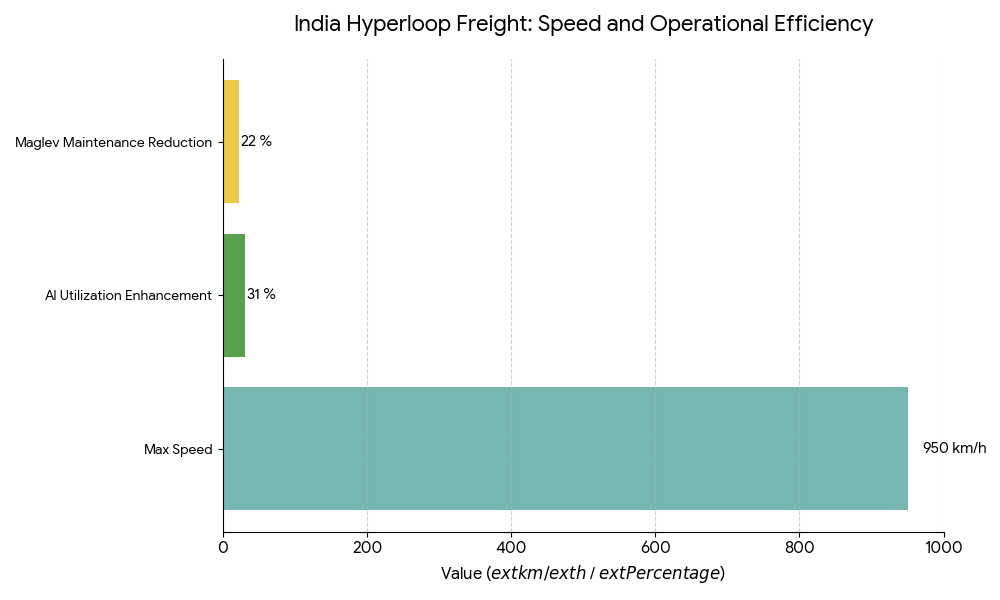

The feasibility outlook for Hyperloop freight in India is driven by rapid urbanization, infrastructure congestion, and net-zero logistics targets. The Mumbai–Pune corridor, once operational, could transport up to 3,000 tons/hour at speeds nearing 950 km/h. Capital expenditure (CAPEX) for pilot deployment is projected between $7B and $9B, inclusive of station infrastructure, safety tunnels, and renewable power grids. AI-driven cargo routing systems are expected to enhance capacity utilization by 31%, while magnetic levitation systems could reduce maintenance costs by 22%. India’s Department for Promotion of Industry and Internal Trade (DPIIT) is finalizing a Hyperloop regulatory sandbox to test design, safety, and certification frameworks. Regional collaboration with Singapore and Japan aims to integrate supply chain analytics and digital twin models for real-time performance tracking. As freight congestion costs India nearly $14B annually, Hyperloop corridors promise a paradigm shift in long-haul cargo logistics, positioning India as a pioneer in Asia-Pacific sustainable freight innovation.

Trends & Insights

- Speed Advantage: Transit times reduced by 85% vs. trucking.

- Renewable Power Integration: 100% clean energy planned for pilot routes.

- AI Cargo Management: 31% improvement in network throughput efficiency.

- Carbon Neutral Goals: 60% CO₂ reduction from freight corridors.

- Feasibility Partnerships: Collaboration between Virgin Hyperloop, DP World, and NITI Aayog.

- Material Innovation: Lightweight carbon fiber tubes reduce costs by 12%.

- Financing Models: 60:40 public-private investment ratio.

- Cross-Border Cooperation: India–Singapore trade corridor feasibility in 2028.

- Digital Twins: Predictive maintenance reduces downtime by 27%.

- E-Commerce Enablement: Hyperloop to cut intercity parcel delivery time to under 2 hours.

These developments underline Hyperloop’s emergence as a high-efficiency freight disruptor redefining India’s logistics architecture.

Segment Analysis

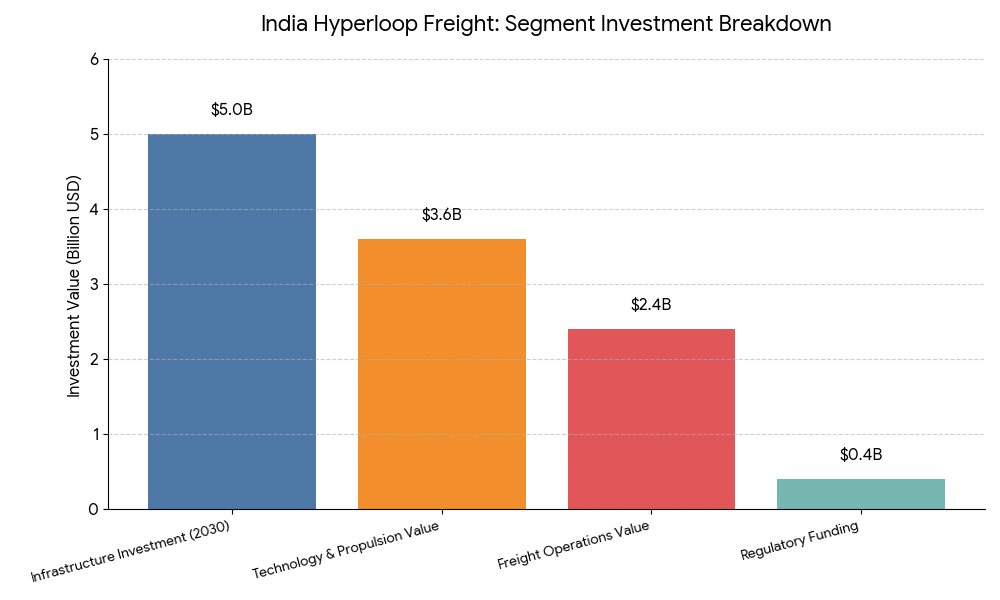

The market divides into infrastructure (40%), technology & propulsion systems (30%), freight operations (20%), and regulatory feasibility (10%). Infrastructure investments, totaling $5B by 2030, include tube alignment, propulsion track installation, and energy management systems. Technology and propulsion, valued at $3.6B, involve linear induction motors, vacuum pumps, and AI-based traffic management. Freight operations, estimated at $2.4B, will focus on automated loading systems and digital route scheduling. The regulatory segment, led by DPIIT and NITI Aayog, is funding $400M for safety and interoperability testing. High-value cargo sectors—pharma, electronics, and perishables—are likely early adopters due to faster cycle times. The overall payback horizon is projected at 12–15 years, contingent on cargo throughput scaling and PPP project execution efficiency.

Geography Analysis

India dominates the regional feasibility market with 47% of Asia-Pacific Hyperloop R&D, followed by Singapore (18%), Japan (14%), and South Korea (11%). The Mumbai–Pune corridor leads India’s pilot deployment, while Delhi–Jaipur and Bengaluru–Chennai are in the pre-feasibility stage. Singapore’s HyperPort model for port-to-air freight interconnectivity is being evaluated for Indian SEZs. Japan’s Shinkansen operators are advising on safety certification frameworks, while Thailand and Malaysia assess regional network integration for intra-ASEAN cargo trade. India’s western logistics belt, home to 85% of export-oriented manufacturing, will serve as the core economic zone for initial Hyperloop operations. By 2030, India aims to link 12 major freight terminals through Hyperloop corridors, reducing delivery times by up to 80% and achieving a 60% drop in emission intensity per ton-km.

Competitive Landscape

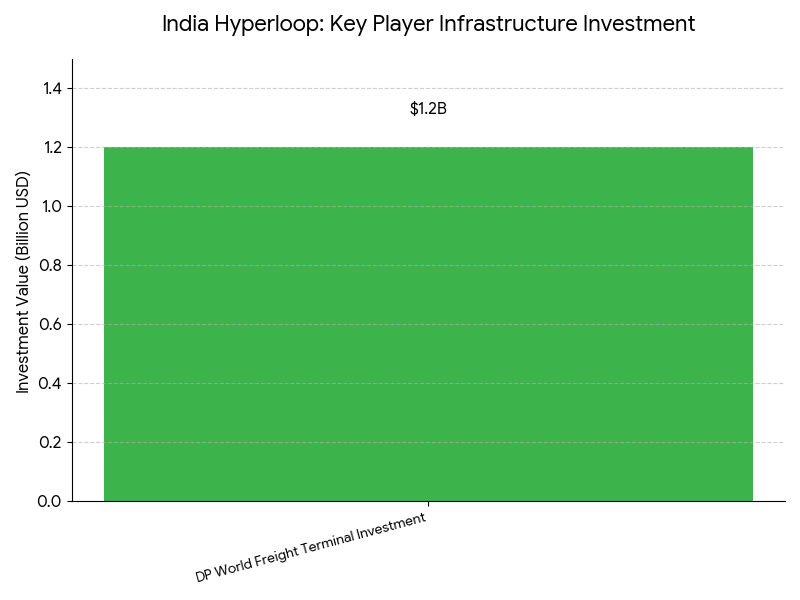

Key players include Virgin Hyperloop, Tata Projects, DP World, HTT (Hyperloop Transportation Technologies), and Siemens Mobility, leading prototype and infrastructure R&D. Virgin Hyperloop India spearheads feasibility testing under Maharashtra’s logistics modernization plan, while DP World commits $1.2B toward freight terminal infrastructure. Siemens Mobility and L&T Technology Services are developing AI-driven cargo scheduling and propulsion analytics. The government’s PPP model is attracting foreign institutional investors, including Temasek Holdings and Japan Bank for International Cooperation (JBIC). Emerging startups, like Ultrain Rail Systems, are piloting cost-efficient vacuum tube materials. Competition is focused on energy optimization, infrastructure modularity, and regulatory readiness, positioning India and Southeast Asia as the global front-runners for Hyperloop-enabled cargo transformation.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071