68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Europe Battery Electrolyte Additives Market Analysis 2025–2033: Racing Toward USD 1 Billion | 12.7% CAGR | Stringent Emissions Drive Demand

The Europe battery electrolyte additives market is projected to grow from USD 440 million in 2025 to nearly USD 1 billion by 2033, at a CAGR of 12.7%. The surge is driven by EV adoption mandates, stringent EU emission norms, and rising investment in gigafactories across Germany, France, and Sweden. Additives such as VC (vinylene carbonate), FEC (fluoroethylene carbonate), and LiDFOB are critical for enhancing electrochemical stability, SEI layer formation, and cycle life in lithium-ion batteries. With Europe’s aggressive shift toward net-zero mobility, electrolyte additive innovation is becoming pivotal for improving battery safety, longevity, and low-temperature performance.

What's Covered?

Report Summary

Key Takeaways

- Market to expand from USD 440M (2025) to USD 1B (2033) at 12.7% CAGR.

- EV production in Europe to exceed 16 million units annually by 2033.

- VC and FEC additives together account for 55% of total additive consumption.

- Germany, France, and Sweden to represent 65% of regional demand.

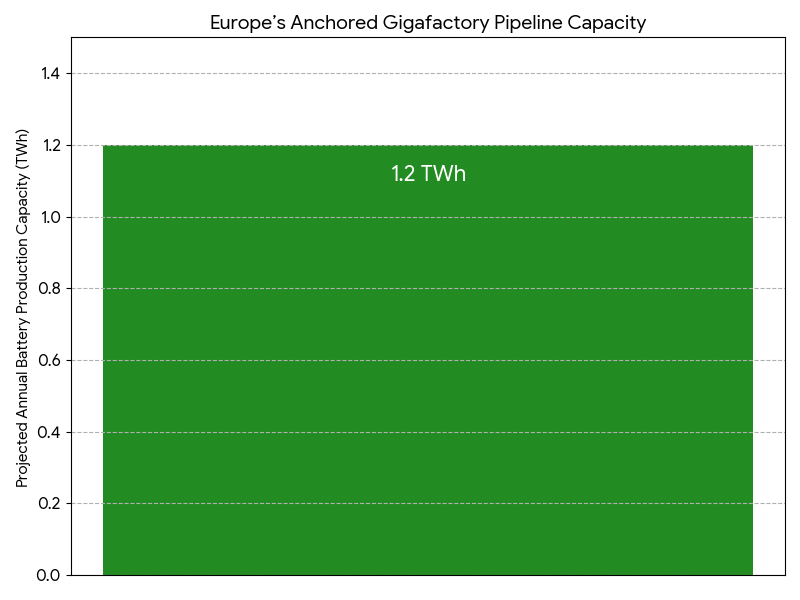

- Gigafactory capacity across Europe expected to surpass 1.2 TWh by 2033.

- Solid-state battery R&D boosting next-gen additive formulations.

- Electrolyte purity standards tightened under EU Battery Regulation (2027).

- Additive localization to reduce import reliance from Asia by 35%.

- Low-temperature and fast-charging additives seeing 18%+ annual growth.

- Circular economy focus driving additive recovery and recycling programs by 2030.

Key Metrics

Market Size & Share

The market will scale from USD 440M in 2025 to USD 1B by 2033, driven by Europe’s expanding EV and energy storage ecosystems. Germany, hosting major gigafactories like Tesla Berlin, Northvolt, and CATL Erfurt, leads demand with 30% market share. France (20%) and Sweden (15%) follow, supported by strong government incentives and advanced R&D hubs. VC and FEC additives dominate, serving as essential SEI enhancers in high-energy-density cells. Rising localization efforts by BASF, Arkema, and Solvay aim to minimize Asia-sourced dependency. The transition to low-flammability and fluorinated additives is a defining trend shaping long-term market share distribution.

Market Analysis

Europe’s aggressive decarbonization targets under the European Green Deal and Fit-for-55 initiative are catalyzing demand for battery-grade chemicals. Additives are critical in extending battery cycle life, reducing gas generation, and enabling ultra-fast charging. The region’s 1.2 TWh gigafactory pipeline anchored by Northvolt, ACC, and Verkor—is amplifying additive procurement. Solid-state battery R&D, notably in Germany and the UK, is generating new demand for lithium phosphate and polymer-compatible additives. Local production capacity is expanding, with Arkema’s FEC plant in France and BASF’s electrolyte additive unit in Ludwigshafen reducing dependency on imports. Rising investments in recycling technologies ensure sustainable additive recovery, aligning with EU’s circular manufacturing mandates.

Trends & Insights

- Regulatory Tightening: EU Battery Regulation to mandate additive traceability by 2027.

- Fluorinated Additives Surge: Demand for FEC and LiDFOB rising in high-voltage cells.

- Local Supply Expansion: European chemical majors scaling domestic additive synthesis.

- EV Growth Catalyst: >16M EVs projected annually, amplifying electrolyte consumption.

- Solid-State Innovation: Additives enabling high ionic conductivity and stability.

- Thermal Safety Priority: Formulation of non-flammable additive systems.

- R&D Alliances: OEMs and universities co-developing next-gen battery chemistries.

- Circular Economy: Solvent and additive recycling integrated into cell manufacturing.

- Cross-Border Partnerships: France–Germany collaborations in battery chemicals R&D.

- Export Potential: EU to become net exporter of battery additives by 2031.

Segment Analysis

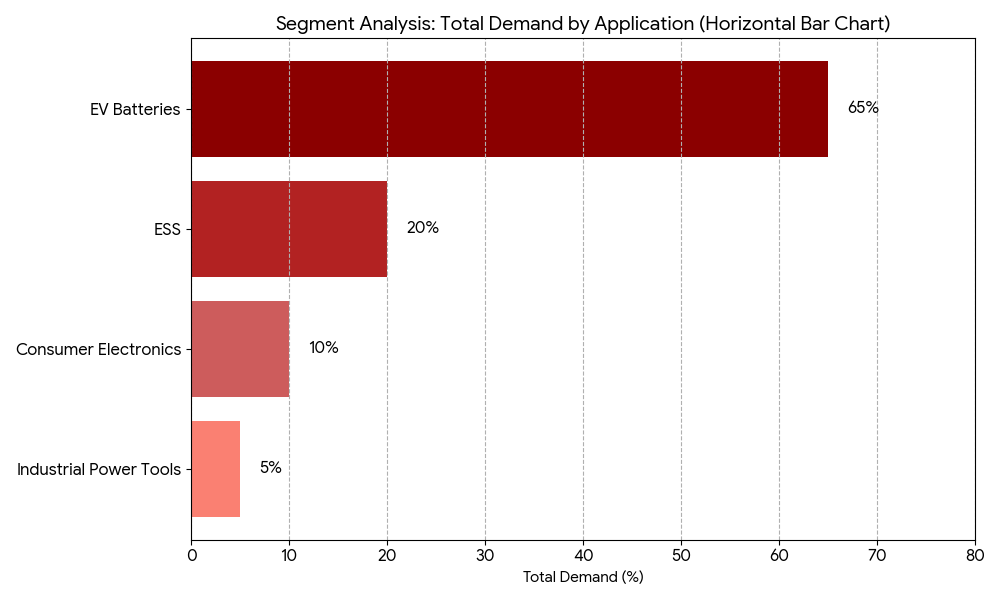

By chemistry, VC (30%), FEC (25%), LiDFOB (15%), PS and PES-based additives (10%), and others (20%) define the composition. VC and FEC dominate lithium-ion systems due to their superior SEI formation and film stability, essential for long cycle life. By application, EV batteries (65%) lead demand, followed by ESS (20%), consumer electronics (10%), and industrial power tools (5%). The solid-state additive segment, though nascent, is growing at 20% CAGR, supporting next-gen battery chemistries. Thermal-stability and fast-charging formulations are gaining traction in high-nickel cathode systems.

Geography Analysis

Germany spearheads the market, contributing 30% of Europe’s additive demand due to automotive dominance and in-region gigafactories. France follows, leveraging state-backed funding for electrolyte innovation, while Sweden benefits from Northvolt’s vertically integrated battery supply chain. Poland and Hungary are rising hubs for cathode and electrolyte production, supported by EU Innovation Fund grants. Italy and Spain are expanding EV battery assembly plants, creating downstream additive opportunities. By 2033, Central and Northern Europe will collectively account for over 70% of market demand, driven by large-scale electrification and supply-chain localization.

Competitive Landscape

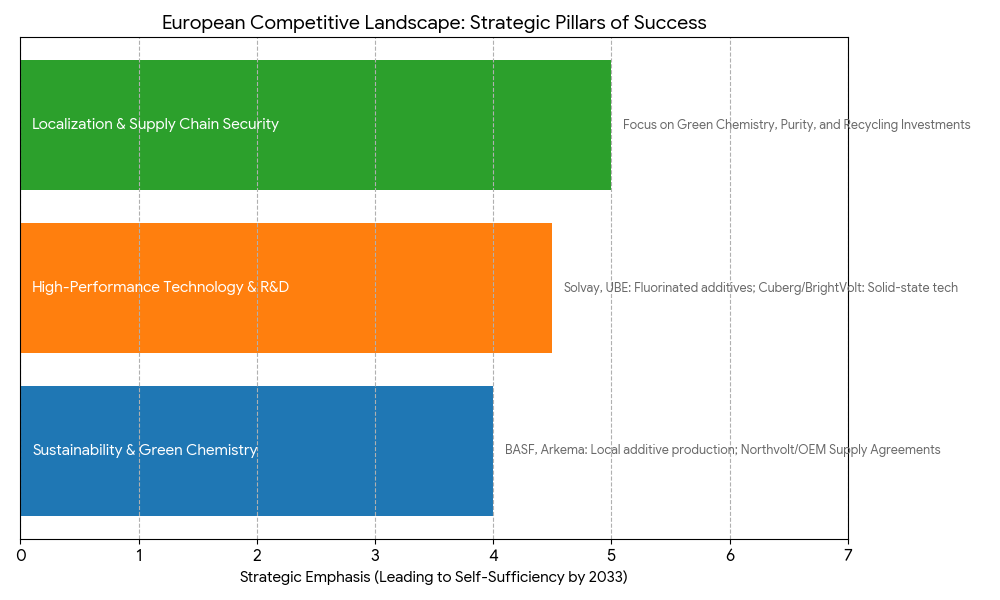

Key market participants include BASF SE, Arkema, Solvay, 3M, Mitsubishi Chemical, UBE Corporation, and Songwon Industrial. BASF and Arkema lead in localized additive production, while Solvay focuses on fluorinated additive R&D for high-voltage electrolytes. UBE and Mitsubishi Chemical supply advanced carbonate-based precursors to European OEMs. Northvolt, ACC, and Verkor have established long-term supply agreements with additive producers for localized procurement. Startups like Cuberg and BrightVolt are entering the market with solid-state-compatible additive technologies. The competitive landscape emphasizes green chemistry, purity, and performance optimization, reinforcing Europe’s drive toward a sustainable, self-sufficient battery materials ecosystem by 2033.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071