68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Embedded Finance for Industrial B2B: Instant Trade Credit, Payments & Risk Rating APIs (US & EU, 2025–2030)

From 2025 to 2030, industrial B2B commerce in the US and Europe will be reshaped by embedded finance that integrates credit, payments, and risk assessment directly into procurement and ERP systems. This shift will replace manual checks with instant underwriting and milestone-based payments, expanding embedded finance volumes to nearly $285 billion in the US and $260 billion in Europe. Growth will be driven by supply-chain resilience, real-time data from open banking and logistics telemetry, and marketplace digitization. While Europe benefits from PSD2/3 frameworks, the US leverages card-based hybrids and real‑time payments toward the same API‑driven financing future.

What's Covered?

Report Summary

Key Takeaways

• Risk‑rating APIs fuse ERP, logistics, and bank data for continuous underwriting.

• Instant trade credit and milestone‑based payouts compress DSO and reduce disputes.

• EU gains from standardized A2A rails; USA blends RTP with card‑rail hybrids.

• Marketplaces/SaaS become primary distribution for embedded B2B finance.

• Tokenized receivables diversify liquidity and price credit dynamically.

• CFO dashboards shift to live cash‑conversion and supplier‑health metrics.

• Data‑governance and audit trails are crucial for regulator and lender trust.

• Winners productize interoperability: ERP, TMS/WMS, e‑invoice, and bank APIs.

Key Metrics

Market Size & Share

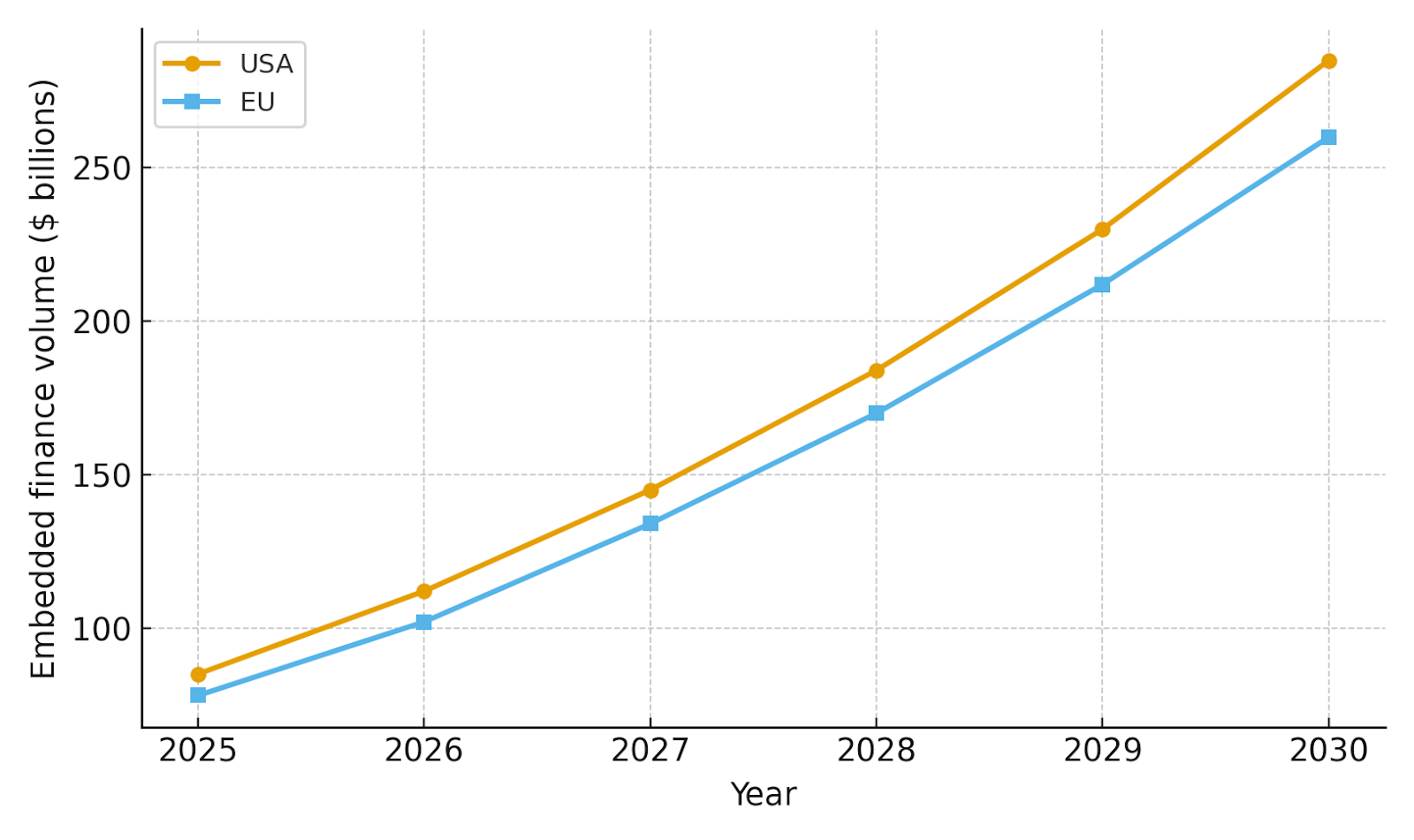

Embedded finance routed through industrial platforms scales rapidly through 2030. The USA expands from ~$85B to ~$285B, driven by marketplace penetration in MRO/metals/chemicals and ERP‑embedded payables/receivables finance. The EU grows from ~$78B to ~$260B aided by instant‑payment coverage and open‑banking data portability. Share remains balanced: the USA leads absolute volumes; the EU keeps pace through standardized rails and cross‑border trade. Competition intensifies among platforms that can demonstrate measurable DSO compression and lower loss rates.

Share drivers include procurement digitization depth, ERP integration coverage, and lender participation. Vendors that expose transparent pricing and auditable data flows win trust with CFOs and credit committees.

Market Analysis

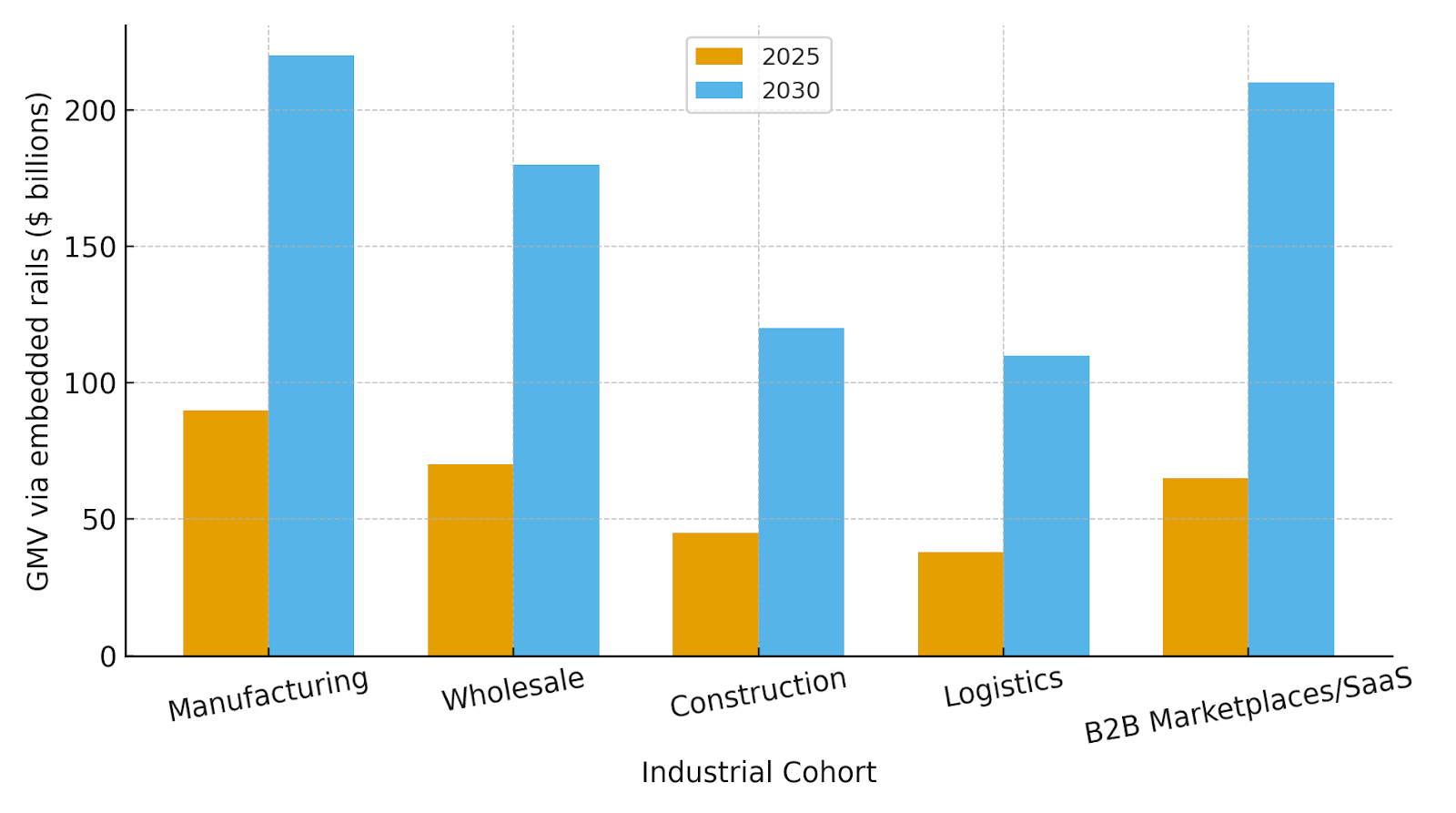

Manufacturing and wholesale dominate embedded finance GMV by 2030, reflecting dense supplier networks and predictable order cycles. Construction adoption accelerates as milestone‑based payouts, retention management, and bonding integrate with underwriting. Logistics networks benefit from shipment‑linked triggers and IoT telemetry, while B2B marketplaces/SaaS play a pivotal distribution role by embedding credit and A2A payments into procurement flows. Across cohorts, API‑level risk signals replace static credit files; credit is priced at order level with eligibility and limits refreshing on each event.

Buyer priorities: lower total cost of capital, fewer disputes and write‑offs, and automated reconciliation to ERP/GL. Lenders prioritize data quality, audit trails, and standardized contracts to syndicate credit efficiently.

Trends & Insights

• Continuous underwriting using ERP events, shipment status, and bank account telemetry.

• Instant‑payment rails (A2A/RTP) used for milestone‑based payouts and automated reconciliation.

• Tokenized receivables enable secondary markets and dynamic credit pricing.

• ESG & supplier‑health analytics folded into credit decisions and procurement SLAs.

• Decision hubs unify pricing, risk, and reconciliation with clear KPIs and SLAs.

• Interoperability becomes table‑stakes: ERP, TMS/WMS, e‑invoice, logistics, and bank APIs.

• Fraud/dispute tooling integrates evidence (PoD, IoT, EDI) to reduce leakage.

• Standardized audit packs improve regulator and lender confidence.

Segment Analysis

• Manufacturing: Supplier‑finance and dynamic discounting at PO/ASN/invoice milestones; strong ERP coverage.

• Wholesale Distribution: Catalog‑driven credit activation; multi‑supplier limits and quick eligibility refresh.

• Construction & Materials: Milestone/retention‑aware payouts; bonding and lien‑waiver workflows integrated.

• Logistics: Shipment‑triggered payments and fuel/maintenance credit; telematics for risk control.

• B2B Marketplaces/SaaS: Primary distribution for embedded credit, A2A payments, and risk APIs; data network effects.

Cross‑segment success depends on measurable DSO reduction, fewer disputes, and lender participation depth.

Geography Analysis

The USA represents ~48% of 2030 embedded finance volume, reflecting market scale and platform penetration. The Euro Area contributes ~36% on the back of instant payments (SEPA Inst) and open‑banking mandates; the UK & Nordics add ~10% with high API adoption; CEE & Others provide ~6% as regional marketplaces scale. Geography influences rail choice EU skews to A2A; USA blends RTP with card hybrids yet both converge on automated reconciliation and continuous underwriting at the order level.

Competitive Landscape

Competitors span (1) vertical B2B marketplaces; (2) ERP‑embedded finance modules; (3) banks and fintech lenders; (4) payment providers integrating A2A/RTP; and (5) credit/identity data networks. Differentiation rests on data coverage (ERP, logistics, bank feeds), speed and explainability of underwriting, dispute/fraud tooling, and transparent economics. Expect consolidation around platforms that deliver live cash‑conversion analytics, risk‑rating APIs, and auditable data pipelines for lenders and regulators.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

$ 1450

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071