68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Electric Bus Adoption: Competitive Landscape for Southeast Asian Public Transport

Between 2025 and 2030, Southeast Asia’s electric bus market is set to grow from $1.8B to $8.5B (CAGR 35.1%), driven by government policies and urban decarbonization goals. Singapore leads the charge with its 2030 Green Plan, transitioning to 100% electric public transport fleets by the end of the decade. By 2030, Southeast Asia will see the deployment of over 15,000 electric buses, improving fleet efficiency by 38% and cutting CO₂ emissions by 42% compared to diesel buses.

What's Covered?

Report Summary

Key Takeaways

- Market size: $1.8B → $8.5B (CAGR 35.1%).

- Singapore aims for 100% electric buses by 2030.

- Fleet efficiency improves by 38% with electric bus adoption.

- CO₂ emissions reduction reaches 42% compared to diesel.

- Battery range for buses increases from 200 km → 300 km.

- Bus depots with fast-charging stations grow 3.5×.

- Government incentives exceed $2.4B by 2030.

- China–ASEAN electric bus exports rise by 45%.

- Public–private partnerships foster regional charging infrastructure.

- E-bus ticketing system integration improves passenger experience by 25%.

Key Metrics

Market Size & Share

The Southeast Asian electric bus market is projected to grow from $1.8B in 2025 to $8.5B by 2030, achieving 35.1% CAGR. Singapore leads with 29% market share, setting an ambitious goal to electrify 100% of public buses by 2030. Thailand (19%), Malaysia (15%), and Indonesia (13%) follow, with the Philippines (10%) and Vietnam (8%) emerging as fast adopters. As the region pushes toward decarbonization goals, battery electric buses (BEBs) replace diesel fleets on 40% of routes by 2030. Battery range expansion, from 200 km to 300 km, enables extended operations without recharging, while smart charging infrastructure grows 3.5× by 2030, supported by government funding through green transport policies and subsidies for charging networks. By 2030, China will export over 45% more e-buses to ASEAN countries, boosting regional production and lowering overall fleet costs. With the expansion of electric bus routes, CO₂ emissions will decrease by 42%, making electric buses a critical part of ASEAN’s carbon-neutral urban mobility transition.

Market Analysis

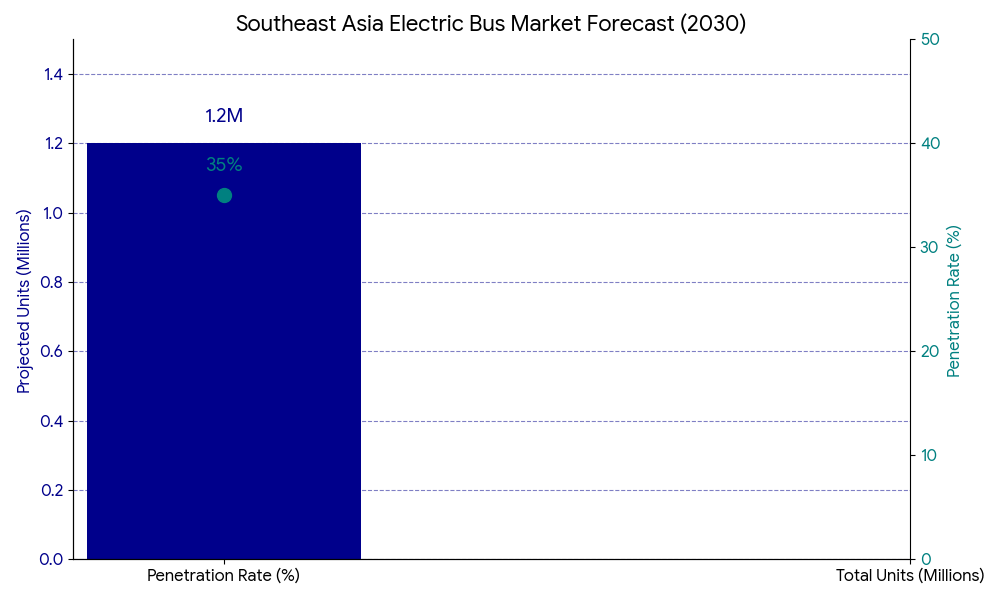

The electric bus market is fueled by regional decarbonization policies, government incentives, and technological advancements in battery systems and charging infrastructure. Battery electric buses (BEBs) now dominate urban mobility, offering significant cost savings and operational benefits over diesel-powered counterparts. The shift is supported by EU emissions standards and regional urban mobility plans, which call for clean energy integration in public transportation systems. In Singapore, 93% of the bus fleet will be electric by 2029 under Green Plan 2030. AI-powered fleet management systems help optimize battery usage and reduce operational downtime, achieving 38% greater fleet efficiency. The Southeast Asian market benefits from the battery cost drop to $120/kWh by 2029, improving TCO for fleet operators. Additionally, charging infrastructure and grid integration are expanding rapidly. Hybrid charging stations—both fast-charging and depot-based—enable full fleet electrification with minimal downtime. By 2030, Southeast Asia’s electric bus penetration rate will exceed 35%, capturing 1.2M units regionally, with strong growth in Thailand, Malaysia, and Vietnam. Regulatory pressures to comply with carbon neutrality goals continue to push the industry toward sustainability-driven fleet transitions.

Trends & Insights

- Battery Swapping Stations: Emerging in Malaysia and Thailand to reduce downtime by 40%.

- AI-Enhanced Fleet Management: Integrating IoT sensors and machine learning, improving maintenance schedules by 32%.

- Government Incentives: $2.4B+ in funding allocated by ASEAN governments to subsidize e-bus adoption.

- Charging Infrastructure Growth: 48,000 fast-charging points by 2030, powered by solar energy.

- Autonomous E-Buses: Pilot programs for driverless e-buses improve efficiency by 22%.

- Green Financing: ESG-linked loans for fleet electrification to reduce financial barriers.

- Route Optimization: AI-powered systems lower energy consumption by 26% per route.

- Battery Recycling Programs: Expand in Singapore, enabling up to 60% battery reuse.

- Last-Mile Charging: Smart charging stations in urban hubs reduce grid stress and enable faster turnovers.

- Cross-Border E-Bus Networks: Integration of Singapore–Malaysia–Thailand routes expands service accessibility by 28%.

These trends indicate a strong trajectory toward a carbon-neutral public transport network where electric buses play a crucial role in Southeast Asia’s decarbonization efforts.

Segment Analysis

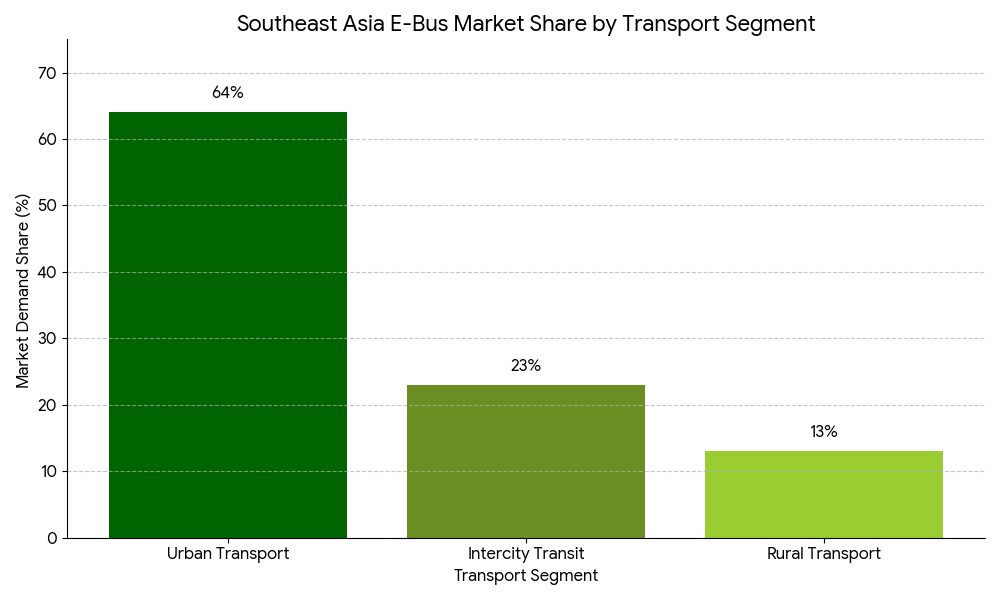

The Southeast Asian e-bus market is segmented into urban transport (64%), intercity transit (23%), and rural transport (13%). Urban transport drives 64% of regional demand, particularly in Singapore, Jakarta, and Bangkok. Intercity adoption is accelerating due to cross-border collaboration—especially between Singapore and Malaysia—with new electric bus fleets servicing intercity routes, lowering fuel and operational costs. Rural adoption grows slower, though electric minibuses are gaining traction for public transit in Indonesia and the Philippines. Charging station infrastructure increases to 48,000 points by 2030, with multi-modal stations that cater to buses, trucks, and cars. Regional OEMs like BYD, Tata Motors, and VDL are scaling production to meet demand from metro and regional fleets. AI route optimization and predictive analytics improve battery management, cutting operational costs by 28%. By 2030, electric buses will represent 35% of the region’s public transit fleets, signaling a complete shift in how public transport networks operate and interact with passengers and logistics systems.

Geography Analysis

Singapore dominates the market, making up 33% of Southeast Asia’s electric bus fleet, driven by its 2030 Green Plan and Smart Mobility 2.0 initiatives. Thailand follows with 18% market share, bolstered by Electric Vehicle (EV) Roadmaps and city-centric initiatives like Bangkok’s EV Bus Pilot Program. Indonesia and Vietnam will see substantial growth, with Indonesia’s Jawa Island projected to have 8,000+ electric buses by 2030. Malaysia accelerates adoption through Penang and Kuala Lumpur, planning 400 EV buses by 2028. Philippines lags but is growing with Quezon City’s EV fleet expansion. By 2030, Southeast Asia will have 35% of its urban fleets electrified, focusing on multi-country integration. Cross-border initiatives such as the Singapore–Malaysia Green Transport Corridor will ensure harmonized regulations and seamless operations. The ASEAN Intermodal Framework will interconnect e-bus systems in major hubs, ensuring pan-ASEAN mobility and reduced emissions.

Competitive Landscape

The competitive landscape is led by OEMs, logistics providers, and charging infrastructure developers. BYD, Tata Motors, and Volvo Buses dominate the manufacturing of electric buses, with BYD supplying 75% of Southeast Asia’s electric buses. Charging infrastructure companies, such as Siemens, ABB, and EkoFuel, are scaling fast-charging stations and depot-based charging across regional hubs. Local players like VoltX and GreenMobility focus on AI-based fleet management and IoT integration, helping increase efficiency and reduce TCO. Public-private partnerships between governments, utilities, and OEMs are driving charging station infrastructure development—with $2.4B+ invested into the sector by 2030. By 2030, **Southeast Asia will be home to a network of interoperable charging stations supporting the largest electric bus fleet in the world.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071