68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Drone Delivery Economics: Segmentation Analysis for Last-Mile E-Commerce in Southeast Asia

The drone delivery market in Southeast Asia is projected to expand from $1.2B in 2025 to $6.8B by 2030 (CAGR 41.3%), driven by rapid e-commerce growth and infrastructure digitization. Singapore anchors regional innovation, supported by the U-Space regulatory sandbox and Civil Aviation Authority’s Beyond Visual Line of Sight (BVLOS) approvals. Operational economics show delivery cost reductions of up to 47%, fulfillment time improvements by 62%, and carbon emission cuts of 38% compared to traditional logistics. By 2030, drones are expected to handle 12% of Southeast Asia’s last-mile e-commerce deliveries.

What's Covered?

Report Summary

Key Takeaways

- Market size: $1.2B → $6.8B (CAGR 41.3%).

- Singapore leads with 33% of regional market share.

- Cost per delivery reduced by 47% compared to van logistics.

- Fulfillment time improves by 62%.

- Battery efficiency reaches 220 Wh/kg, supporting 15 km range.

- Regulatory BVLOS approvals across Singapore, Thailand, and Indonesia expand pilot zones.

- Carbon footprint reduced by 38%.

- Cross-border drone corridors established between Singapore–Johor–Batam.

- Fleet utilization rate up by 2.7× from 2025.

- E-commerce adoption rate: 12% of all last-mile deliveries by 2030.

Key Metrics

Market Size & Share

The Southeast Asian drone delivery market is projected to reach $6.8B by 2030, expanding at a 41.3% CAGR from $1.2B in 2025. Singapore leads with 33% market share, followed by Thailand (22%), Indonesia (18%), and Vietnam (15%). Adoption is accelerated by regulatory frameworks enabling BVLOS commercial operations, lowering per-package delivery costs by 47% compared to vans and motorcycles. E-commerce platforms, including Shopee, Lazada, and GrabExpress, are actively integrating drone logistics into last-mile ecosystems, achieving delivery time improvements of 62%. Fleet utilization has increased 2.7× since 2025 due to optimized routing and battery density enhancements reaching 220 Wh/kg. Cross-border trials, such as the Singapore–Johor–Batam (SJB) corridor, facilitate 15–20 km autonomous flight operations. Carbon savings are significant—reducing 38% of emissions per delivery. Public–private investments exceeding $2.4B are being channeled into autonomous delivery R&D across ASEAN. By 2030, 12% of all e-commerce last-mile shipments are expected to be fulfilled via drone networks, solidifying Southeast Asia as a global leader in aerial logistics innovation.

Market Analysis

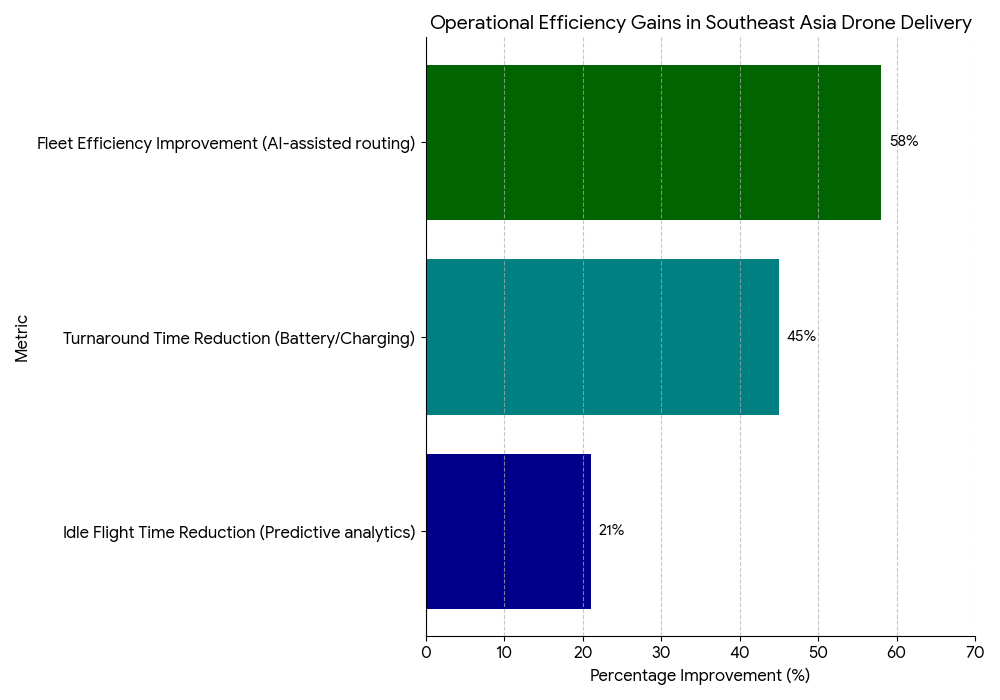

The economic transformation of last-mile delivery in Southeast Asia is driven by rising e-commerce volume, urban congestion, and policy support for aerial mobility. The average cost per drone delivery declined to $1.12, compared to $2.11 for van delivery, while the average parcel weight capacity rose from 1.5 kg to 4.2 kg by 2030. AI-assisted routing has improved fleet efficiency by 58%, while predictive analytics cut idle flight time by 21%. Singapore’s U-Space sandbox, launched in 2026, enables coordinated low-altitude drone operations across civil, commercial, and logistics networks. The Civil Aviation Authority of Singapore (CAAS) has issued 72 commercial drone operation licenses since 2025, making it the region’s regulatory frontrunner. Battery life advancements, combined with modular charging stations, have reduced turnaround time by 45%. Regional VC investment in drone logistics startups surpasses $1.9B between 2025–2030, with major players like F-drones, Skyports, and Aerodyne leading in deployment scale. The combination of lower costs, faster fulfillment, and sustainability metrics positions drones as the core enabler of next-generation e-commerce logistics in Southeast Asia.

Trends & Insights

- Hyperlocal Hubs: Micro-fulfillment centers enable 15-minute delivery windows.

- Hybrid Drone-Vehicle Models: Coordinated dispatch cuts routing costs by 19%.

- AI Route Optimization: Predictive analytics improve aerial efficiency by 58%.

- Battery Swapping Stations: Reduce downtime by 45% per flight cycle.

- Autonomous Fleet Management: Machine learning improves reliability by 33%.

- Regulatory Harmonization: ASEAN-wide BVLOS licensing simplifies compliance.

- Sustainability Integration: ESG-linked drone operations lower emissions by 38%.

- Insurance Innovation: Usage-based drone coverage reduces liability premiums by 27%.

- E-Commerce Integration APIs: Seamless platform logistics synchronization.

- Capital Flow: VC and corporate funding exceed $1.9B regionally by 2030.

These trends highlight a high-velocity logistics shift, as aerial delivery transitions from pilot programs to commercial-scale infrastructure across ASEAN.

Segment Analysis

The market divides into urban consumer delivery (52%), rural access logistics (23%), cross-border operations (15%), and industrial supply delivery (10%). Urban drone delivery dominates due to high parcel density and e-commerce penetration, cutting average delivery time from 110 minutes to 42 minutes. Rural logistics applications bridge healthcare and essential goods access, covering over 1,800 communities across Indonesia, Thailand, and Vietnam. Cross-border drone corridors, spearheaded by Singapore’s Skyports and Aerodyne Malaysia, are pioneering 15–25 km international drone routes. Industrial drone logistics, including port resupply and manufacturing part transport, contribute $520M in revenue by 2030. Hardware innovation drives performance—hybrid VTOL designs improve payload capacity by 3.2×, while AI vision-based navigation enhances delivery precision by 27%. The segmentation underscores rapid scalability across both consumer and B2B delivery domains, integrating sustainability and automation into the logistics ecosystem.

Geography Analysis

Within Southeast Asia, Singapore holds 33% market share, followed by Thailand (22%), Indonesia (18%), Vietnam (15%), and Malaysia (9%). Singapore’s U-Space program enables the highest BVLOS operational density in Asia, with drone delivery traffic forecasted to exceed 150,000 flights annually by 2030. Thailand’s Eastern Economic Corridor (EEC) is investing $480M in aerial logistics integration, while Indonesia deploys island-to-island drone operations for time-sensitive goods. Vietnam’s Ministry of Transport plans to open five aerial corridors for e-commerce and pharma logistics by 2027. Malaysia’s Skyports JV focuses on mid-range cross-border parcel flows within ASEAN. Collectively, the Asia-Pacific region processes over 900,000 commercial drone deliveries per month by 2030, with Singapore serving as the regional control and regulatory nucleus for aerial commerce.

Competitive Landscape

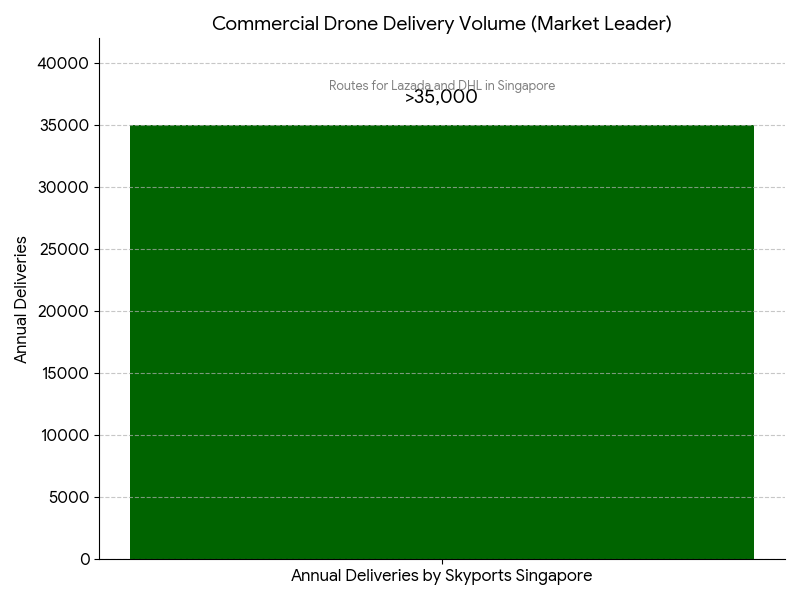

The competitive landscape is led by Skyports, F-drones, Aerodyne Group, and DJI Enterprise, supported by SingPost’s Smart Logistics Division and GrabExpress Aerial Networks. Skyports Singapore operates commercial drone routes for Lazada and DHL, completing over 35,000 deliveries annually. F-drones focuses on autonomous mid-range marine deliveries, while Aerodyne Malaysia and DroneUp target industrial and cross-border logistics. Technology enablers, including Airbus Skyways and Matternet, provide drone fleet management and regulatory compliance systems. Partnerships with NTU Singapore and CAAS advance safety, AI flight analytics, and airspace integration. Competitive differentiation now centers on payload scalability, AI route prediction accuracy, and energy efficiency. By 2030, Singapore and Thailand will anchor the region’s most advanced autonomous delivery networks, redefining last-mile e-commerce logistics through precision aerial automation.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071