68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Digital Transformation in Indian Freight Management: Growth Opportunities - Segmentation Analysis

Between 2025 and 2030, India’s digital freight management market is projected to grow from $6.9B to $22.7B (CAGR 27.4%), driven by rapid adoption of AI-based transport planning, IoT telematics, and blockchain-enabled logistics visibility. Government programs such as GatiShakti, ULIP (Unified Logistics Interface Platform), and National Logistics Policy (NLP 2030) are integrating multimodal transport data across road, rail, air, and sea networks. Digitization is projected to reduce freight delays by 38%, optimize fleet utilization by 26%, and cut logistics costs as a share of GDP from 14% to 9.8% by 2030, reinforcing India’s position as Asia’s next major logistics powerhouse.

What's Covered?

Report Summary

Key Takeaways

- Market size: $6.9B → $22.7B (CAGR 27.4%).

- Logistics cost-to-GDP ratio declines from 14% → 9.8%.

- Digital freight platforms adoption grows 4.5×.

- ULIP integration covers 90% of multimodal data nodes by 2030.

- AI-based routing optimization reduces delays by 38%.

- Fleet utilization efficiency improves by 26%.

- Blockchain visibility platforms reduce disputes by 42%.

- E-waybill automation adoption reaches 94% of national shipments.

- Freight emissions intensity cut by 23% through green route planning.

- SME logistics digitization up 3.7×, driven by SaaS freight tools.

Key Metrics

Market Size & Share

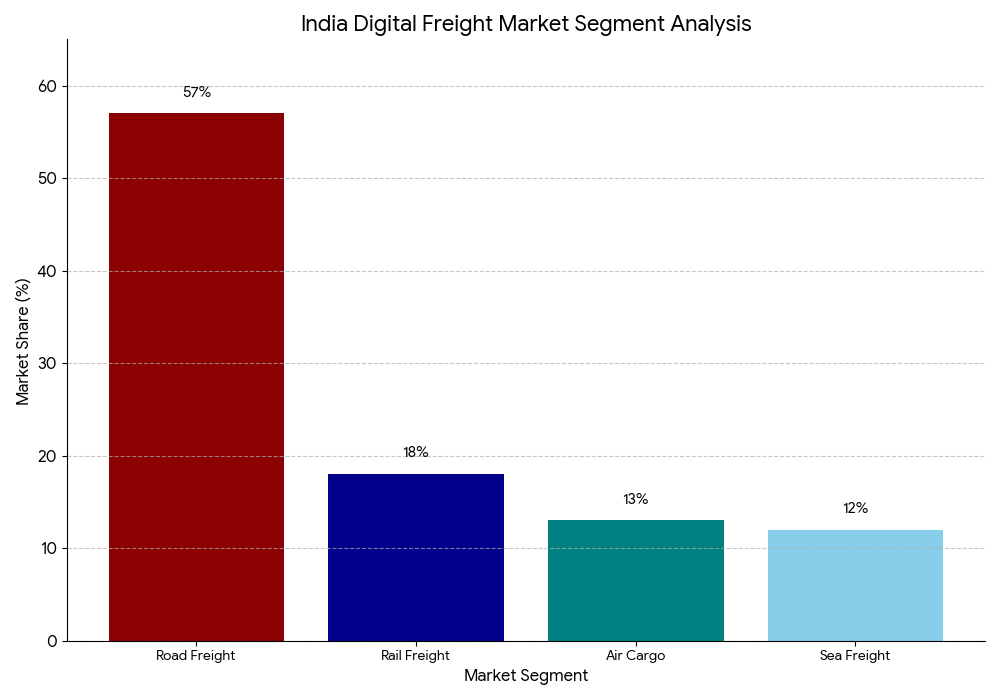

India’s digital freight management sector will expand from $6.9B in 2025 to $22.7B by 2030, marking a 27.4% CAGR. This growth is driven by widespread digitization across surface transport (57%), rail freight (18%), air cargo (13%), and port logistics (12%). Government-led frameworks like ULIP and GatiShakti are centralizing freight data for real-time route and asset visibility, reducing overall freight cycle time by 38%. SME freight adoption through platforms such as Freight Tiger, BlackBuck, and Rivigo 2.0 accelerates automation in truck scheduling, freight payments, and e-waybill processing. Large-scale warehouse integration, including Amazon, Delhivery, and TCI Express, supports multimodal load balancing across corridors like Delhi–Mumbai and Bangalore–Chennai. India’s logistics cost, which stood at 14% of GDP, is projected to decline to 9.8% by 2030 due to improved data interoperability and automation efficiency. AI-based route optimization, IoT fleet telematics, and predictive freight scheduling will deliver cost savings exceeding $18B annually. As India transitions toward a fully digital logistics network, its freight sector will become a model of data-driven efficiency within the Asia-Pacific trade ecosystem.

Market Analysis

India’s freight ecosystem is undergoing a rapid digital infrastructure transformation, bridging efficiency gaps across transport and logistics. Government initiatives like the Unified Logistics Interface Platform (ULIP) integrate data from over 36 government systems, offering real-time multimodal visibility. Digital freight platforms, such as Freight Tiger and Kale Logistics, are redefining procurement and capacity utilization, reducing idle time by 22% and enabling paperless workflows. AI-based predictive routing enhances time-definite deliveries by 38%, while telematics-driven monitoring improves fleet uptime by 25%. Blockchain-enabled visibility platforms eliminate 42% of documentation disputes, enhancing transparency in trade compliance. The AI & IoT integration wave is attracting over $2.1B in venture funding from 2025–2029. On the policy front, the National Logistics Policy (NLP) and PM GatiShakti are targeting a logistics performance index improvement from 44th to 25th globally by 2030. The integration of smart warehousing systems, predictive analytics, and cloud-based transport exchanges is expected to increase freight throughput by 33%, enhancing India’s global competitiveness as a manufacturing and export hub.

Trends & Insights

- Data Interoperability: ULIP unifies freight data across road, rail, air, and ports for seamless tracking.

- Predictive Freight Planning: AI algorithms improve delivery accuracy by 32%.

- E-Waybill Automation: Digital documentation cuts compliance costs by 27%.

- Smart Fleet Maintenance: IoT sensors extend asset lifespan by 22%.

- Digital Payments in Freight: Instant settlements reduce DSO (days sales outstanding) by 36%.

- Sustainability Compliance: Route optimization reduces CO₂ emissions by 23%.

- Tech Consolidation: Logistics SaaS platforms attract $2.1B in VC funding.

- Private–Public Collaboration: GatiShakti partnerships enhance infrastructure throughput.

- Customs API Integration: Accelerates port clearance by 35%.

- AI Load Optimization: Boosts container utilization by 19%.

These trends position India as Asia-Pacific’s most digitized and resilient freight economy, where real-time data and analytics are redefining logistics efficiency.

Segment Analysis

The digital freight market divides into road freight (57%), rail freight (18%), air cargo (13%), and sea freight (12%). Road freight digitization dominates, led by BlackBuck and Delhivery, automating over 80% of route scheduling. Rail logistics, under DFCC (Dedicated Freight Corridors), integrates digital terminals improving asset turnaround by 28%. Air cargo platforms, including CargoFlash and Kale Galaxy, digitize 90% of air waybills, cutting ground processing time by 25%. Port logistics, modernized through Port Community Systems (PCS 2.0), expands digital container visibility across 13 major ports, boosting throughput by 21%. SME adoption of logistics SaaS tools accelerates through affordable TMS platforms, offering dynamic rate discovery and digital payments. The segment’s transformation supports India’s shift toward multimodal efficiency, linking inland logistics seamlessly with global trade nodes. By 2030, over 60% of India’s freight movement will be digitally orchestrated, marking the transition to a smart, unified logistics economy.

Geography Analysis

Within Asia-Pacific, India commands 61% of regional digital freight revenue, followed by Indonesia (17%), Thailand (10%), and Vietnam (8%). Domestically, Maharashtra, Gujarat, and Tamil Nadu lead digital logistics adoption, representing 47% of total freight digitization. Northern industrial corridors—especially Delhi–Mumbai and Eastern Freight Corridors—achieve real-time multimodal visibility via ULIP and RFID-based e-tracking. Southern India emerges as the AI innovation hub, housing startups in Bangalore and Hyderabad focused on fleet optimization and predictive scheduling. Port modernization in Mundra, Chennai, and Vizag digitizes cargo handling with IoT sensors. Cross-border collaboration under India–ASEAN logistics partnerships expands export visibility across Thailand, Malaysia, and Singapore. By 2030, India’s digitally enabled freight networks will interconnect over 1.2M vehicles and 40,000 warehouses, establishing Asia’s most advanced real-time logistics grid.

Competitive Landscape

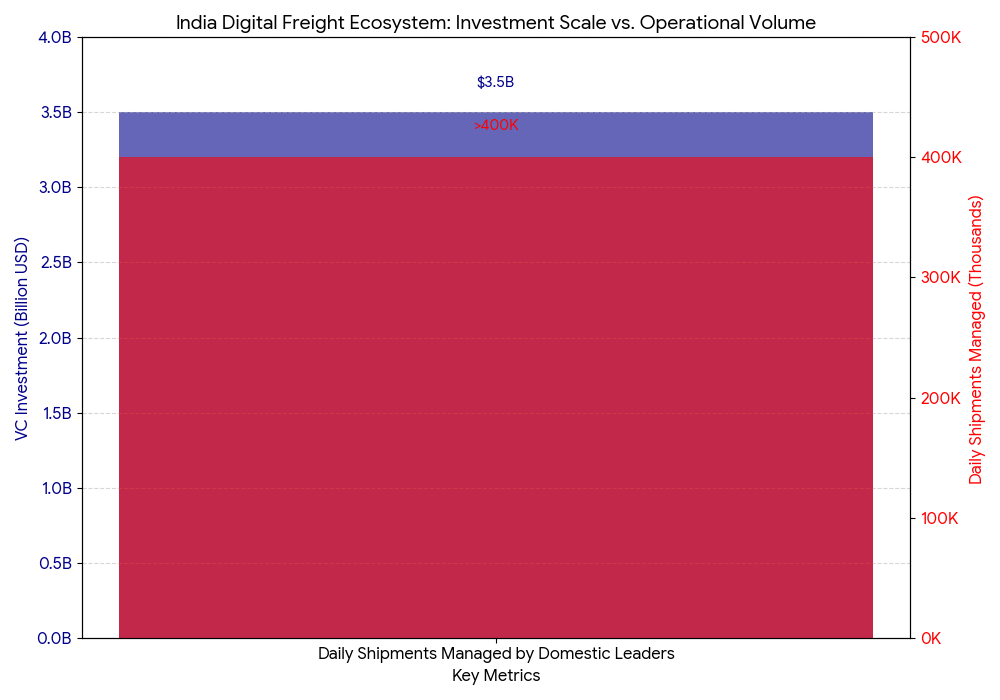

The competitive landscape includes digital freight marketplaces, TMS providers, and analytics-driven 3PLs. BlackBuck, Delhivery, and Freight Tiger dominate domestic markets, managing over 400,000 daily shipments. Kale Logistics and CargoFlash lead in airport and port digitalization, while TCI Express and Mahindra Logistics invest in AI-based route optimization. Tech enablers such as SAP Transportation Management, FarEye, and LogiNext power predictive analytics for large enterprises. Global players like Maersk, DP World, and DHL Supply Chain are integrating with ULIP APIs to ensure compliance and visibility. Venture capital investment, crossing $3.5B since 2025, accelerates innovation in freight SaaS and IoT telematics. Competitive advantage now depends on data accuracy, real-time visibility, and ESG alignment, positioning India as the digital freight transformation benchmark for Asia-Pacific logistics modernization.\

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071