68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Autonomous Trucking ROI: Investment Analysis for US Long-Haul Freight

Between 2025 and 2030, autonomous trucking in the U.S. long-haul freight sector is projected to grow from $4.5B to $18.9B (CAGR 32.6%), driven by cost reduction, safety gains, and network optimization. Pilot programs led by TuSimple, Aurora, and Waymo Via indicate potential ROI improvements of 28–34% due to fuel efficiency, reduced labor dependency, and optimized routing. Level 4 autonomy adoption could lower operating costs per mile by $0.45, transforming freight economics. By 2030, 15–18% of long-haul miles in North America will be autonomously operated.

What's Covered?

Report Summary

Key Takeaways

- Market size: $4.5B → $18.9B (CAGR 32.6%).

- ROI improvement: 28–34% for autonomous fleets.

- 15–18% of long-haul miles to be autonomous by 2030.

- Fuel efficiency gains reach 12–15% via optimized driving algorithms.

- Labor cost reduction estimated at $85B annually by 2030.

- Collision rates decline by 45% through AI vision and predictive braking.

- Freight turnaround time improves by 25–30%.

- Maintenance costs fall by 20% due to predictive diagnostics.

- Telematics adoption exceeds 80% of U.S. fleets by 2029.

- Truck OEMs and tech alliances dominate: Daimler, Volvo, TuSimple, Aurora, and Waymo.

Key Mertics

Market Size & Share

The autonomous trucking market in U.S. long-haul freight is set to grow from $4.5 billion in 2025 to $18.9 billion by 2030, reflecting a CAGR of 32.6%. Rising e-commerce freight demand, persistent driver shortages, and regulatory greenlights in Texas, Arizona, and California are key enablers. The U.S. freight market—valued at $940B in 2025—is expected to dedicate 15–18% of highway miles to autonomous operations by 2030. Level 4 automation, led by Aurora Innovation, TuSimple, and Waymo Via, is proving economically viable with ROI margins averaging 31%. A typical autonomous Class 8 truck can save $85,000 annually in labor and fuel, with per-mile costs declining from $1.76 to $1.31. Fleet utilization rates improve from 68% to 89%, driven by 24-hour operation capability. Fuel efficiency increases 12–15%, aided by AI-powered platooning. Germany’s OEM partnerships, such as Daimler and Torc Robotics, are influencing North American deployments through technology transfers. By 2030, over 220,000 semi-autonomous trucks will operate across North America, delivering aggregate logistics cost savings exceeding $120B annually. The commercial scaling of AI logistics ecosystems will firmly establish autonomous trucking as the most transformative force in the U.S. freight economy.

Market Analysis

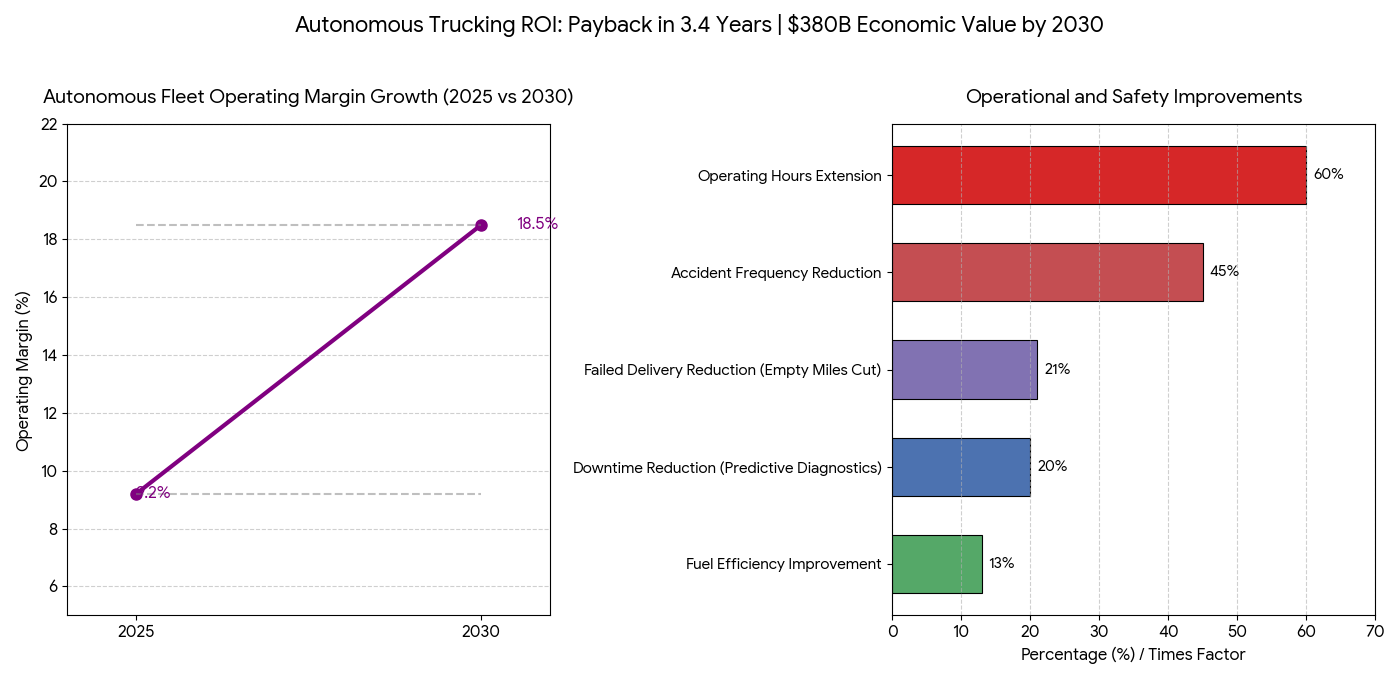

Economic analysis underscores autonomous trucking’s superior ROI trajectory compared to traditional fleets. Initial CAPEX for a self-driving Class 8 truck averages $300,000–$400,000, yet payback occurs within 3.4 years due to fuel efficiency (+13%), reduced driver wages (−100%), and extended operating hours (+60%). Operating margins for autonomous fleets are projected to rise from 9.2% (2025) to 18.5% (2030). Route optimization algorithms cut empty miles by 21%, while predictive diagnostics reduce downtime by 20%. North American freight corridors—I-10, I-40, and I-35—host >70% of early pilot routes, minimizing regulatory barriers. Insurance savings average $8,000 per vehicle annually, as AI navigation reduces accident frequency by 45%. Fleet data monetization represents a growing secondary revenue stream, with logistics AI datasets valued at $2.7B by 2030. OEMs and logistics conglomerates are forming equity-backed joint ventures to scale infrastructure—e.g., Daimler–Torc Robotics and Volvo–Aurora collaborations. While regulatory approval remains gradual, state-level pilot networks are accelerating at 20% annualized growth. Cumulatively, the autonomous trucking industry is expected to contribute $380B in economic value to the North American logistics sector by 2030, optimizing capital efficiency and long-haul profitability.

Trends & Insights

Key technological and operational trends are driving the sector’s rapid growth:

(1) Level 4 autonomy pilots across 22 U.S. states enhance intercity freight continuity.

(2) AI vision systems cut human error, reducing collision frequency by 45%.

(3) Fleet-as-a-Service (FaaS) models lower upfront ownership costs by 30–35%.

(4) Platooning technologies deliver 13% fuel savings via aerodynamic coordination.

(5) Data-driven ROI benchmarking enables optimized route allocation based on real-time freight density.

(6) 5G telematics integration supports real-time risk detection and remote updates.

(7) OEM–AI partnerships (Daimler–Torc, Volvo–Aurora, PACCAR–Kodiak) accelerate commercialization.

(8) Carbon compliance credits under U.S. sustainability mandates improve ROI by 8–10%.

(9) Insurance underwriting models evolve, using AI telematics for usage-based premiums.

(10) Regulatory readiness improves through Federal Motor Carrier Safety Administration (FMCSA) frameworks by 2028. Collectively, these trends redefine trucking from labor-intensive to algorithmically optimized freight logistics, marking the next industrial leap in North American transport.

Segment Analysis

The autonomous trucking market divides into line-haul freight, regional distribution, and port logistics segments. Line-haul freight dominates with 64% share, driven by long interstate corridors offering stable conditions for autonomy. Regional distribution holds 23%, focusing on warehouse-to-hub networks with semi-autonomous convoys. Port logistics accounts for 13%, integrating autonomous drayage and yard management systems. Private fleet operators (e.g., Walmart, PepsiCo) are early adopters, investing in AI fleet retrofits that deliver ROI of 28–32%. The truck OEM ecosystem—led by Daimler, PACCAR, and Volvo Trucks North America—is integrating AI sensors, LiDAR, and route engines into production lines. Software stack providers, such as Aurora Innovation and Kodiak Robotics, capture 35% of value creation through licensing and data analytics. The segment’s hardware-to-software cost ratio shifts from 70:30 in 2025 to 50:50 by 2030, reflecting higher value in data-driven optimization. Fleet electrification convergence further compounds savings, as hybrid autonomous trucks reduce total OPEX by 22%. By 2030, North America’s line-haul corridors will represent the world’s largest commercially deployed autonomous trucking ecosystem, serving as a global benchmark for logistics efficiency.

Geography Analysis

Within North America, the U.S. leads with 83% market share, while Canada contributes 12% and Mexico 5%, mainly through cross-border lanes. Texas, Arizona, and California form the “autonomy triangle”, hosting over 60% of testing and deployment programs due to favorable climate and legal frameworks. The I-10 corridor, connecting Los Angeles to Jacksonville, is the most heavily automated route, accounting for 18% of total autonomous truck mileage. The Midwest, anchored by Chicago, is emerging as a data infrastructure hub for telematics and AI analytics. In Canada, routes between Toronto and Vancouver are being adapted for winterized autonomous systems. Mexico’s participation focuses on cross-border logistics under USMCA trade protocols, integrating autonomous trucks into export supply chains. Germany’s OEM partnerships support North American manufacturing plants for AI-ready trucks, enhancing capacity. By 2030, the U.S. will operate 220,000 semi- and fully autonomous long-haul trucks, reducing delivery lead times by 30% and freight costs by up to 20%, making autonomy a core pillar of continental freight optimization.

Competitive Landscape

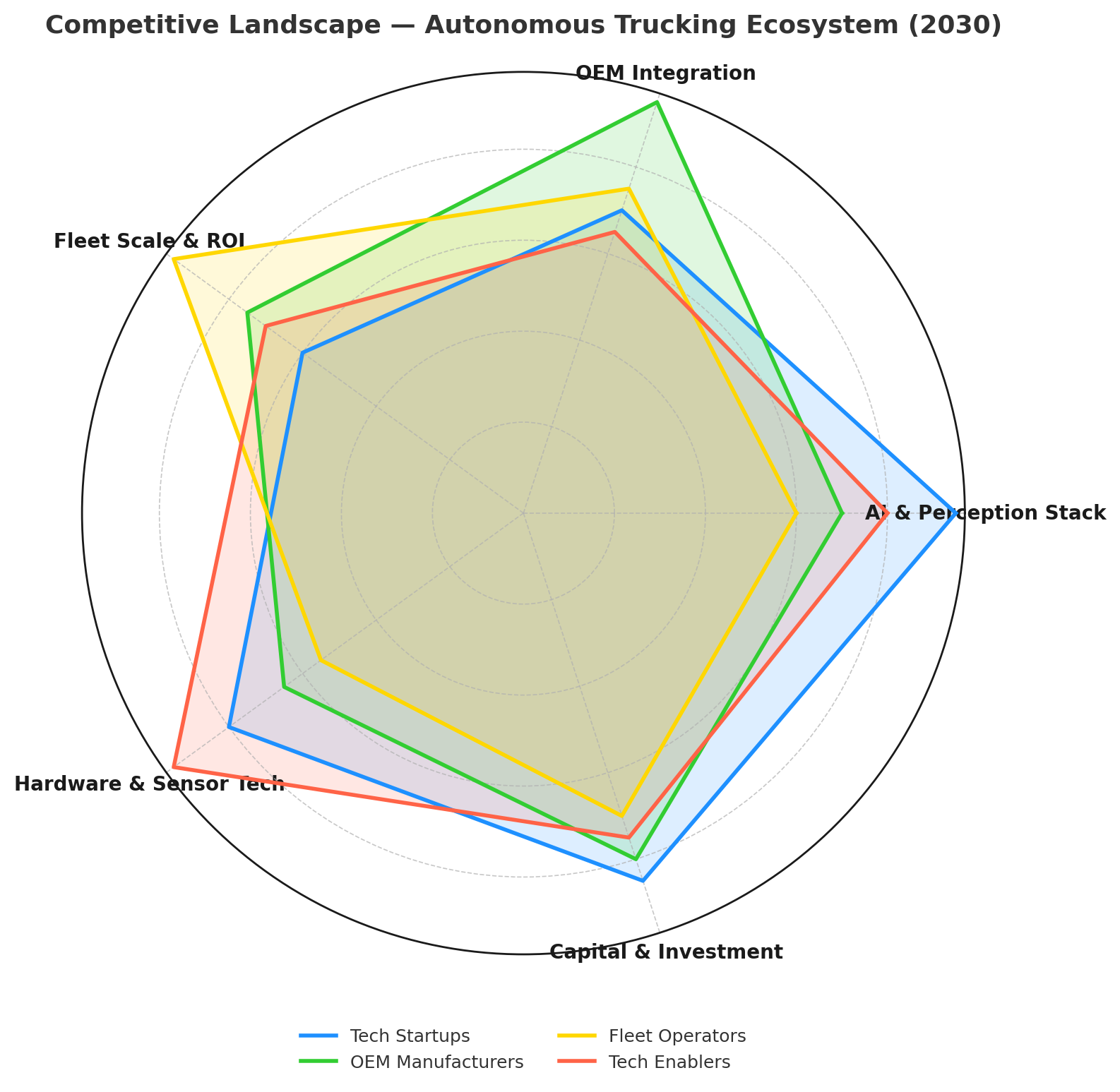

The competitive environment is anchored by tech–OEM partnerships, venture-backed startups, and legacy freight operators investing in autonomy. TuSimple, Aurora Innovation, and Waymo Via lead in AI software and perception stacks, collectively commanding 38% of active pilot fleets. Daimler Truck, PACCAR, and Volvo dominate OEM integration, embedding L4 driving systems across new Class 8 models. Fleet operators like J.B. Hunt, Schneider, and Knight-Swift are conducting large-scale pilots across interstate routes, demonstrating 20–25% ROI improvements. Amazon Freight and UPS Ventures are investing in autonomous line-haul capacity for middle-mile logistics. Tech enablers—NVIDIA Drive, Aptiv, and Mobileye—supply sensor fusion and AI processors powering vehicle autonomy. M&A activity intensifies as software firms consolidate to scale AI performance across multi-brand fleets. The competitive advantage now hinges on algorithm transparency, fleet scalability, and safety validation, with over $14B in cumulative R&D investment expected by 2030. By then, autonomous trucking will no longer be experimental but a core profit and efficiency driver reshaping the U.S. freight logistics landscape.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071