Get in touch with us to learn more about our services, ask for assistance with a technical difficulty, or if you would like a product demo.

info@nextyn.com

Singapore

68 Circular Road, #02-01 049422, Singapore

68 Circular Road, #02-01 049422, Singapore

Jakarta

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Mumbai

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Bangalore

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

Thank you for submitting the form

Oops! Something went wrong while submitting the form.

%20(Black).avif)

Get in touch with us to learn more about our services, ask for assistance with a technical difficulty, or if you would like a product demo.

info@nextyn.com

Singapore

68 Circular Road, #02-01 049422, Singapore

68 Circular Road, #02-01 049422, Singapore

Jakarta

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Mumbai

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Bangalore

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

Thank you for submitting the form

Oops! Something went wrong while submitting the form.

Get in touch with us to learn more about our services, ask for assistance with a technical difficulty, or if you would like a product demo.

info@nextyn.com

Singapore

68 Circular Road, #02-01 049422, Singapore

68 Circular Road, #02-01 049422, Singapore

Jakarta

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Mumbai

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Bangalore

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Thank you for submitting the form

Oops! Something went wrong while submitting the form.

AI-Optimized Credit Card Pricing Strategies: Spend Pattern Analysis & Balance Transfer Incentives - Pricing Strategies

Former Vice President of Payments Product Strategy & GTM

JPMorgan Chase & Co.

Consumer Finance

USA

$ 795

June 2025

Report Summary

- How do ML models segment customers for dynamic APR offers?

- What balance transfer fee structures maximize customer retention?

- How are rewards aligned with individual spending patterns?

- What risk-based pricing tiers comply with fair lending laws?

- How is customer intelligence tools monitor market rates?

- What competitive intelligence tools monitor market rates?

- How do churn prediction models influence pricing decisions?

- What personalization engines deliver real-time offers?

- How are cost of capital fluctuations managed in pricing?

- What profitability metrics validate pricing strategies?

- How do regulatory stress tests impact pricing models?

- What A/B testing frameworks optimize offer acceptance?

Report Keywords

- Dynamic Pricing

- Spend Segmentation

- Balance Transfers

- Rewards Optimization

- Risk-Based Pricing

- Customer Lifetime Value

- Competitive Benchmarking

- Regulatory Compliance

- Churn Prediction

- Personalized Offers

- Cost of Capital

- Profitability Models

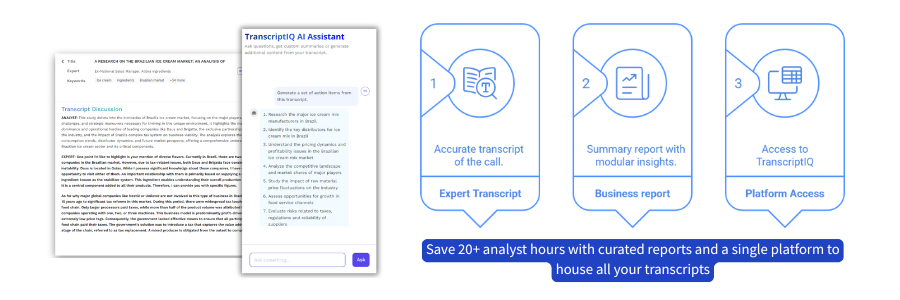

What You get When You Buy This Transcript?

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

Get in touch with us to learn more about our services, ask for assistance with a technical difficulty, or if you would like a product demo.

info@nextyn.com

Singapore

68 Circular Road, #02-01 049422, Singapore

68 Circular Road, #02-01 049422, Singapore

Jakarta

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Mumbai

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Bangalore

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Thank you for submitting the form

Oops! Something went wrong while submitting the form.

Related Transcripts

Bank-as-a-Platform (BaaP) in Europe: API Monetization, Partner Ecosystem Value & Compliance Cost

Former CTO

HSBC

BAAP

API Monetization

Europe

Topics covered in this transcript

Keywords

$ 795

August 2025

Financial Super-Apps in the West: User Growth, Cross-Sell Rates & Revenue per Active User (2025–2030)

Former Senior Director

Visa

Financial Payment App

Cross Sell Rates

Europe

USA

Topics covered in this transcript

Keywords

$ 795

August 2025

Crypto Payment Adoption in EU vs. U.S. Merchants (2025–2030): Volume Growth, Ticket Sizes & Merchant ROI

Former Senior Consultant

PayX Group

Cryptocurrency Adoption

Crypto Paymen Adoption

USA

Topics covered in this transcript

Keywords

$ 795

August 2025

Digital Wallet Saturation in the U.S. & EU: Active User Growth, Merchant Adoption & Per-Transaction Margins (2025–2030)

Former Director

Global Payments Inc.

Digital Payment Systems

USA

Europe

Topics covered in this transcript

Keywords

$ 795

August 2025

FedNow and the Economics of 24/7 Payments: Liquidity Management, Fraud Controls & Cost Models

Former Independent Consultant

J.P. Morgan

FedNow

Economics

USA

Topics covered in this transcript

Keywords

$ 795

August 2025

%20(White).avif)

Expert Transcripts

Our Offices

Singapore

68 Circular Road, #02-01 049422, Singapore

68 Circular Road, #02-01 049422, Singapore

Jakarta

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Bangalore

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Mumbai

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Get in touch with us to learn more about our services, ask for assistance with a technical difficulty, or if you would like a product demo.

info@nextyn.com

Singapore

68 Circular Road, #02-01 049422, Singapore

68 Circular Road, #02-01 049422, Singapore

Jakarta

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Revenue Tower, Scbd, Jakarta 12190, Indonesia

Mumbai

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Bangalore

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Buy Now

Thank you for submitting the form

Oops! Something went wrong while submitting the form.