68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Middle East Lithium-ion Battery Solvent Market Report 2025–2033: From USD 20 Million to USD 82 Million | Explosive 19.1% CAGR

The Middle East lithium-ion battery solvent market is expected to grow from USD 20 million in 2025 to USD 82 million by 2033, reflecting an explosive CAGR of 19.1%. Growth is driven by rapid EV fleet expansion, energy storage system (ESS) deployment, and increasing battery manufacturing localization under regional clean energy programs. Solvents like ethylene carbonate, dimethyl carbonate, and diethyl carbonate are witnessing surging demand due to their role in improving electrolyte conductivity and cycle stability. With large-scale battery gigafactories under construction in Saudi Arabia and the UAE, solvent consumption will rise sharply, solidifying the Middle East’s position as a critical supply-chain hub in the global lithium-ion battery ecosystem.

What's Covered?

Report Summary

Key Takeaways

- Market to rise from USD 20M (2025) to USD 82M (2033) at a 19.1% CAGR.

- Saudi Arabia and UAE together to account for 65% of regional demand.

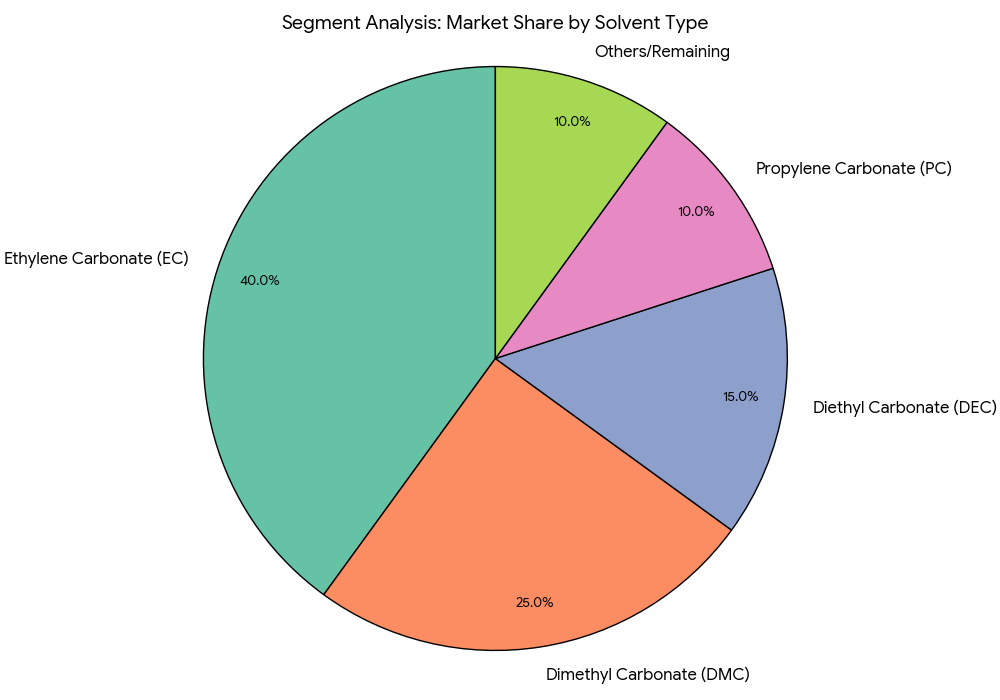

- Ethylene carbonate (EC) remains the dominant solvent, capturing 40% share.

- Battery manufacturing capacity in the GCC to exceed 35 GWh by 2033.

- Electric vehicle (EV) demand in the region to grow 9× between 2025 and 2033.

- Energy storage systems (ESS) to represent 25% of total solvent consumption.

- Local chemical producers scaling output to reduce import dependency (currently 80%).

- Government-backed industrial policies promoting chemical localization under Vision 2030.

- Solvent recycling initiatives expected to cut production costs by 18% by 2032.

- Growing partnerships between Asian electrolyte firms and Middle Eastern energy players.

Key Metrics

Market Size & Share

The Middle East lithium-ion battery solvent market will increase 4.1× between 2025 and 2033, reaching USD 82 million. Saudi Arabia (38%) and UAE (27%) dominate due to their growing EV and grid-scale storage markets. The ethylene carbonate (EC) segment leads, followed by DEC and DMC, collectively representing 80% of demand. Battery-grade solvents are essential in enhancing electrolyte conductivity and safety in lithium-ion cells. As regional gigafactories come online, such as Saudi’s CEER Battery Plant and UAE’s Khalifa Industrial Zone projects, demand for localized, high-purity solvents will surge. Increased investment in chemical clusters and R&D centers is expected to further expand regional production capacity.

Market Analysis

The market’s rapid acceleration aligns with the Middle East’s electrification and industrial diversification agenda. Driven by Vision 2030 and Energy Transition 2050 frameworks, nations are investing in upstream chemical production to reduce raw material import dependency. The GCC’s battery manufacturing capacity is set to reach 35 GWh by 2033, supporting both EV assembly and renewable storage sectors. Demand from ESS installations, expected to account for 25% of solvent use, reflects growing grid modernization needs. Strategic alliances between Asian electrolyte firms (LG Chem, Mitsubishi, Panasonic) and regional companies are fostering technology transfer and joint manufacturing. Furthermore, solvent recycling R&D is projected to lower unit production costs by 18% while improving lifecycle efficiency.

Trends & Insights

- Gigafactory Expansion: Multiple battery plants in Saudi Arabia and UAE driving bulk chemical procurement.

- Localization Efforts: Regional push to build domestic chemical supply chains.

- Solvent Innovation: Development of fluorinated carbonate solvents improving battery safety.

- Hydrogen-Electric Synergy: Integration with fuel cell R&D in Saudi industrial zones.

- Renewable Storage Growth: ESS deployment expanding solvent demand beyond EVs.

- Trade Partnerships: GCC–Asia agreements accelerating material sourcing efficiency.

- Sustainability Focus: Recycling initiatives minimizing solvent waste.

- Government Incentives: Tax breaks and subsidies for chemical processing investments.

- Infrastructure Development: Industrial zones integrating battery and chemical plants.

- Export Potential: By 2033, the Middle East expected to supply 10% of global solvent exports.

Segment Analysis

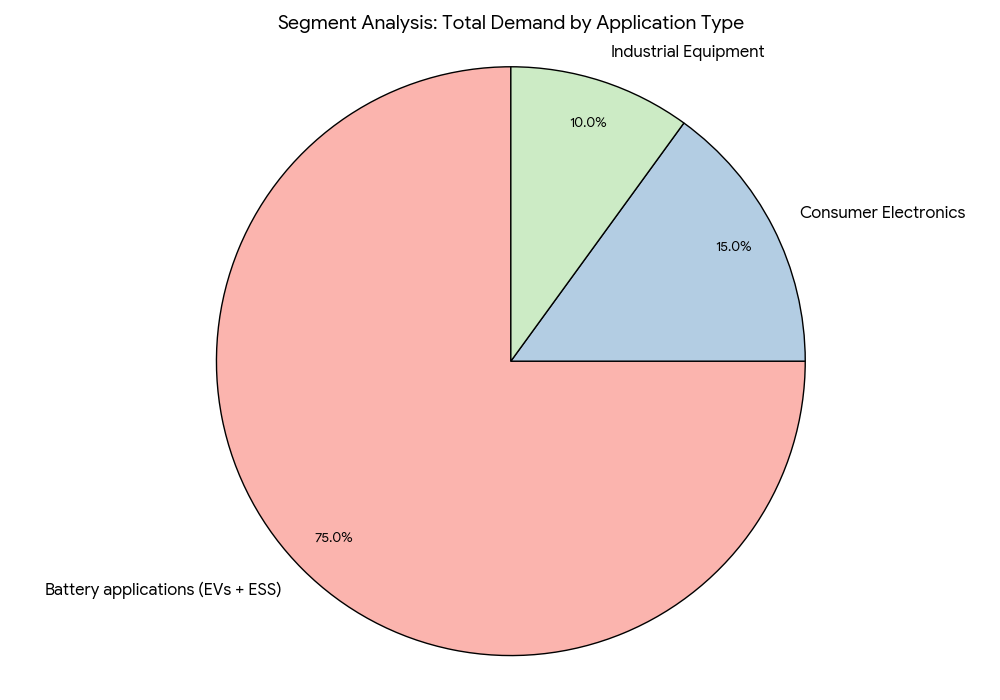

By solvent type, ethylene carbonate (40%), dimethyl carbonate (25%), diethyl carbonate (15%), and propylene carbonate (10%) dominate the market. Ethylene carbonate (EC) remains the solvent of choice due to its high dielectric constant and stability, critical for high-energy-density batteries. Battery applications (EVs + ESS) represent 75% of total demand, followed by consumer electronics (15%) and industrial equipment (10%). The automotive segment leads growth with a 21% CAGR, supported by EV mandates and private fleet electrification programs. Recycling and recovery technologies are emerging as high-growth subsegments, anticipated to attract USD 30M in cumulative R&D investments through 2033.

Geography Analysis

Saudi Arabia leads the market with strong backing from PIF and SABIC, hosting battery chemical hubs in Yanbu and Jubail. UAE follows with industrial expansions in Khalifa Industrial Zone Abu Dhabi (KIZAD), focusing on localized battery electrolyte and solvent production. Oman and Qatar are positioning themselves as logistics and export gateways for chemical trade. Egypt and Morocco are integrating solvent supply into North Africa’s emerging EV manufacturing corridor. Collectively, these efforts position the Middle East as a strategic node for Asia–Europe energy storage supply chains, leveraging proximity, logistics, and renewable energy abundance to achieve cost-competitive chemical manufacturing.

Competitive Landscape

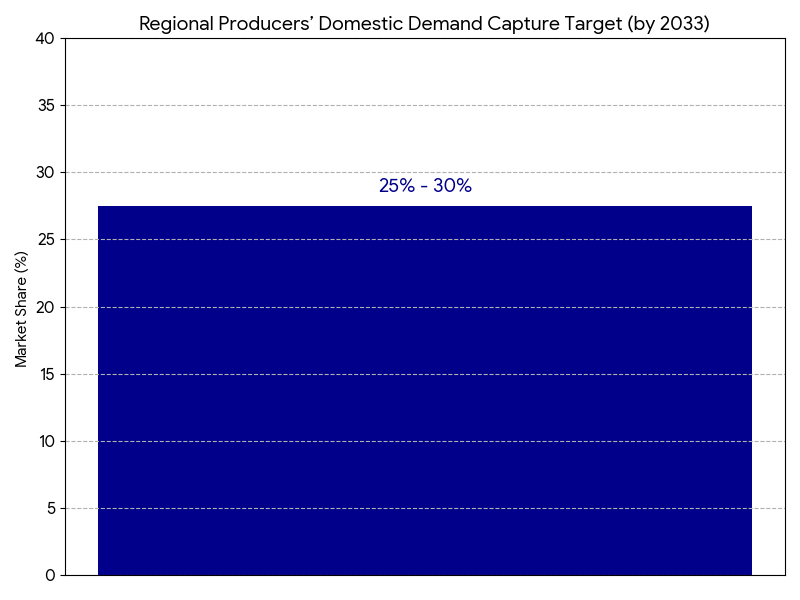

Major market participants include SABIC, Saudi Aramco, ADNOC Refining, Mitsubishi Chemical, LG Chem, UBE Industries, Huntsman, and BASF. SABIC and ADNOC are investing in battery-grade solvent facilities aligned with Vision 2030 localization goals. Mitsubishi Chemical and LG Chem are establishing joint ventures for carbonate solvent production, ensuring quality and supply consistency. UBE Industries is introducing fluorinated carbonate formulations, enhancing electrolyte stability for high-voltage applications. BASF and Huntsman are targeting R&D partnerships in thermal management and recycling. The competitive landscape is defined by integration across upstream feedstocks, electrolyte blending, and recycling, with regional producers expected to capture 25–30% of total demand domestically by 2033.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071